- The Castle Chronicle

- Posts

- Unlocking Hyperliquid: A Deep Dive into its Future and Fair Valuation

Unlocking Hyperliquid: A Deep Dive into its Future and Fair Valuation

ericonomic & Defi Man

February 23, 2024 • Est. Reading Time: 8 minutes

Unlocking Hyperliquid: A Deep Dive into its Future and Its Fair Valuation

A Castle Capital Research Report

⚔️ A Call to Arms

Think you have what it takes to enter the Castle and contribute to research, community initiatives, due diligence analysis, and advising/servicing projects in the space? Or maybe you want to upskill and shadow community members who have already walked a successful path as an intern?

Executive Summary

Hyperliquid is redefining the Perpetual DEX landscape, ranking third in volume behind GMX and DYDX, with over $190m in TVL.

Source: DefiLlama

While perceived as a simple smart contract on Arbitrum, Hyperliquid is, in fact, a dApp-chain, a strategic move for scaling and enhancing platform solvency.

Its unique approach as a dApp-chain enables atomic liquidations, funding distributions, and solvency guarantees at the end of every L1 block, offering a distinct advantage over traditional dApps limited by underlying blockchain infrastructures.

The platform's valuation is tricky without its own token, but its innovative points system hints at a significant valuation, challenging conventional market assessments.

As Hyperliquid progresses toward a token sale and potentially expands its offerings beyond a Perp DEX, its decentralization, security, and scalability approach positions it for substantial growth in the Perp dex market.

Use our referral system to spread the word about the Chronicle!

What people think Hyperliquid is

As mentioned above, Hyperliquid is one of the most widely used Perpetual DEXs. As part of their roadmap, they have hinted that in the near future, the protocol will evolve to become “not just a perp dex,” but unfortunately, we don’t have more information about that yet.

Hyperliquid UX (fast, gasless, and simple), very similar to that offered by a CEX, leads people to think that Hyperliquid is a simple Smart Contract deployed on Arbitrum, where users deposit tokens and can use them without the need to send on-chain transactions (and pay gas) or the need to sign for each transaction.

However, the reality is quite different, as Hyperliquid is a Layer 1, or more precisely, a dApp-chain.

Dappchain vs Dapp

Why a dApp-chain? According to Jeff1 , the leader of The Chameleon (the main Core Contributor of Hyperliquid), it's necessary for a Perp DEX to be built on its L1 if it wants to scale properly.

He cites three main reasons for this:

Liquidate positions atomically with oracle updates.

Distribute funding to every user atomically on the hour.

Guarantee platform solvency at the end of every L1 block.

But why an L1 and not a dApp?

A dApp is an application built on a blockchain, which means it is limited by the underlying infrastructure:

On one hand, dApps have many limitations: they have to pay for gas in a specific token and with an amount dependent on the saturation of that blockchain, adapt to its block speed, use its programming language, etc.

But on the other hand, they have a fundamental advantage: all the infrastructure to build is already in place, including a network of validators/miners, liquidity, etc.

A dApp-chain is not like that; it's built on its blockchain (or Layer 1) and is the only dApp on that blockchain.

A simple analogy to understand this would be comparing a supermarket to a shopping mall: a shopping mall would be a Layer 1 with hundreds of stores (many dApps) inside it; a supermarket is its own establishment (a single dApp).

We can find many examples of both currently:

dApp: Vertex Protocol, GMX, Gains Network

dApp-chain: Hyperliquid, dYdX, Orderly Network

Considering this and taking the hypotheses of the Fat Protocol Thesis2 as references, we will dive into a hypothesis regarding the current and future valuations of Hyperliquid.

Current valuation

Regarding Hyperliquid, it's difficult to estimate its valuation since it (yet) doesn't have its token –- but thanks to its points system, we can estimate some hypotheses.

Their points system works so that 1 million points are distributed weekly for six months, giving 24 million points. To these points, we must add the points from the Alpha version, of which we have no information, but rumors suggest they could be either 1 million (for a total of 25 million) or 6 million (a total of 30 million).

Based on this total number of points and considering that Hyperliquid hasn’t received external funding from VCs, it’s said to be possible that:

Each point is worth one token

The total supply of tokens is 100 million

Therefore, the total airdrop is 25-30% of the total supply

Normally, projects don’t distribute such a large portion of the tokenomics for the airdrop. However, this seems a concrete option, given that Hyperliquid has not received VC funding.

The market is valuing each point at around $3.53 , a price rising since it became available on the public OTC market, giving a total FDV of $350M if the 100M tokens total supply is correct.

If this is true, does this mean the market is correctly evaluating each point of Hyperliquid?

Probably not, mainly because they do not consider that Hyperliquid is not only a dApp, but a dApp-chain.

The Future of Hyperliquid

According to the initial schedule, the point program will end on the 16th of May 2024, and most likely, the airdrop will occur shortly after.

Most details remain unknown, but considering they didn’t raise outside money yet, it would make sense for the Hyperliquid team to set up some sort of public offering of tokens, similar to what Jupiter (JUP) did, to secure some runaway without the need to dump tokens in the market later on.

Under the assumption they will airdrop 25% to early users, keep 35% for the team, and 40% for block rewards & trading incentives, it would make sense for them to secure some of the team allocation while giving willing investors a chance to buy tokens in size at a fair price.

Let’s say 5% out of the team allocation was to be sold to the public at a current potential valuation of $350M FDV, that means the team would raise about $17.5M, which should be easy to fill considering the mindshare Hyperliquid accrued last months.

The Hyperliquid team is small, with just 8 team members, so this raise should give them enough runway for a couple of years without the need to sell any $HL.

As long as the price doesn’t feel excessive (like what happened with $JUP), doing a token sale should not be a problem for the future price action of the token and could even reduce selling pressure in the future (as the team is not forced to sell tokens to sustain development ala Chainlink)

The months following the TGE will be important for the future success of the protocol, as the token deployment will bring some relevant challenges along the way and the opportunity to cement Hiperliquid’s positioning within the perp industry.

While the protocol has achieved great success, current high levels of activity will be hard to maintain, considering that some users are mercenary traders farming the airdrop – which will fly to greener pastures once this happens. Innovative ways to build loyalty among current users and attract more in the future will be needed to stay at the top.

As previously mentioned, Hyperliquid runs on their L1, secured by Proof of Stake, with four existing validators currently run by the team – a centralization issue understandable at this stage but not ideal for the long term.

This will probably change with the token deployment, increasing the number of validators. Future operators will likely need to lock a certain amount of $HL to run the validator in exchange for $HL gas fees, block rewards & part of the fees earned by the protocol.

This decentralization is unequivocally bullish for the long-term health of the protocol as it increases safety and reduces potential centralization issues. This confidence is very important to siphon further traders from CEX to an alternative like Hyperliquid.

This step doesn’t come without challenges, as the increase in security and transparency of a decentralized set of validators might come to the detriment of other features like latency if not handled properly.

Increasing the number of validators usually makes consensus harder and thus increases confirmation times for much worse latency. Adjusting this will surely be one of the leading tech challenges in scaling the protocol.

Additionally, scaling throughput is another important factor to consider. Currently, the Hyperliquid chain supports 20k TPS, which is more than enough at this stage but might not be enough in the future if the number of users grows considerably. The team is already working on the tech stack to allow for higher activity levels without compromising performance.

Lastly, increasing the number of validators could make upgrading the protocol harder. Still, this is not something critical, as Solana has shown there are mechanisms to prevent this from being a big hurdle.

Future valuation

Crypto markets are usually far from rational, making valuations hard to predict. Nonetheless, looking at how the market values perp dexes and the current ceiling in this segment is helpful.

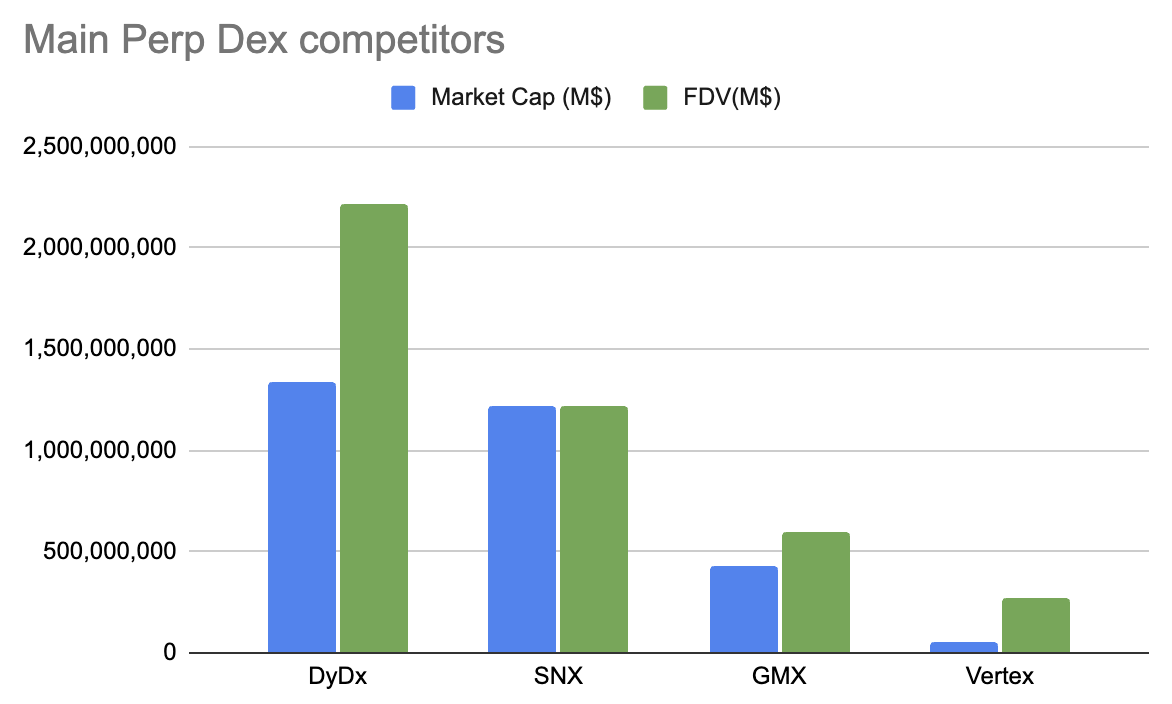

DyDx was the first perpetual DEX to be deployed and has retained the number as one of the spot by trading volumes (even though GMX is the number one by fees) and commands the higher valuation across the segment both in terms of market cap and FDV, sitting at $1.3B and $2.2B.

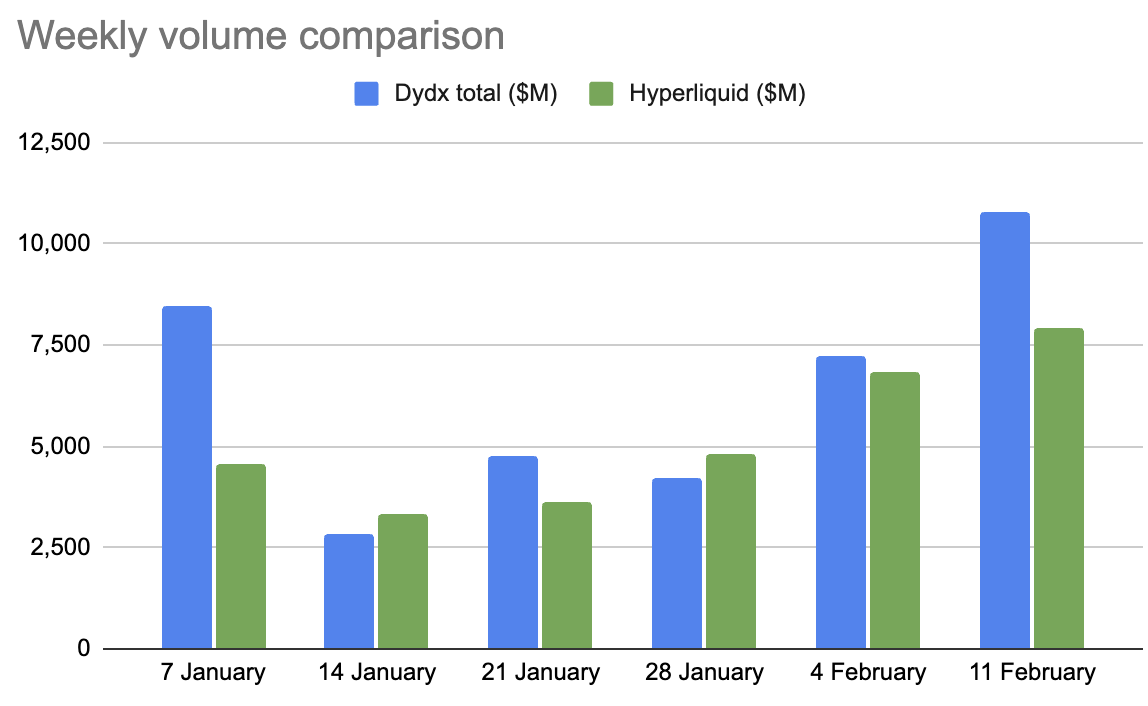

How do Hyperliquid volumes compare with DyDx numbers?

Current volume numbers are very similar, as can be appreciated in the above chart. While some of Hyperliquid volumes are derived from wash-trading to farm the potential airdrop, there are also trading incentives happening at DyDx. Therefore, we believe this will not greatly affect the initial valuation. If the metrics deteriorate substantially after the airdrop, a repricing to the downside could kick in, as happened previously with Vertex.

So, is it realistic to expect the same valuation as DyDx?

Probably not, as battle-tested protocols in DeFi almost always command a premium versus new entrants, but expecting 50% of DyDx FDV seems a reasonable hypothesis.

This translates into expectations of an FDV ceiling of $1.1B and probably an initial trading range between $0.5B-1.1B, due to the selling pressure from airdrop recipients and the inherent volatility of this market.

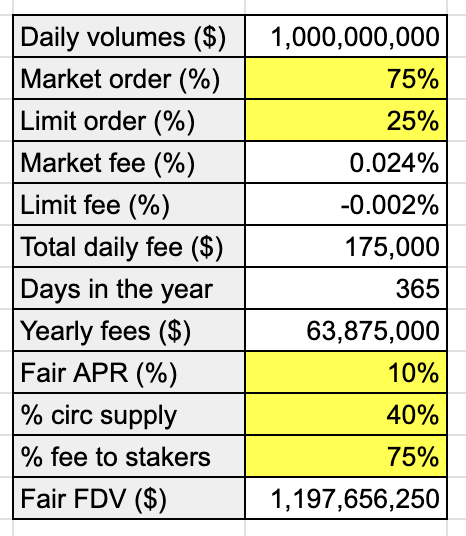

Is that consistent with the fees Hyperliquid is currently generating?

Spoiler: Yes, it is. Running the numbers, we arrive at a very similar conclusion: $1.1B FDV should be the fair value of Hyperliquid.

Details about the numbers can be found in the following table. The main hypotheses are highlighted in yellow and are:

75% of current volumes belong to taker orders that pay 0.024%

25% of current volumes belong to market orders that get paid 0.002%

10% is the APR that $HL stakers receive at a “fair valuation.”

40% is the circulating supply at launch

75% of the fees generated by the protocol are distributed to stakers (while the rest is redirected to the insurance fund etc.)

Hyperliquid also is introducing a fee tier system that will set a different fee depending on the trading volumes of each user (like most CEXes).

The bracket will start at 0.035% taker fees and end at 0.019% taker fees. The bigger the volumes, the smaller the fees. This change will go live on March 10th, so we are not considering it in our calculation.

This projection focuses on “real yield” distributed to stakers and does not consider the rewards that might come from block rewards or gas fees in the form of $HL tokens.

The future valuation of the token after launch will depend a lot on how well Hyperliquid manages to retain its traders and attract more in the future.

Overall, the perp dex segment is poised to grow until the pico top of the cycle due to regulatory issues with CEXes and increased demand in the bull cycle, so Hyperliquid will also benefit from that “tide rising all the boats” effect.

Before concluding, it's interesting to note that Jeff and Hypurr (HL core contributors) hinted4 that Hyperliquid might evolve beyond being merely a Perp DEX. This could alter our expected valuation analysis.

Some possible additions could involve Forex and stock derivatives markets (similar to those in Gains Network) in the future.

We believe the future is bright for Hyperliquid and look forward to seeing them succeed.

Sources:

Jeff, Leader of The Chameleon Core Contributors, Twitter post. https://twitter.com/chameleon_jeff/status/1758121288210481268

"Fat Protocols," Union Square Ventures. https://www.usv.com/writing/2016/08/fat-protocols/

Hyperliquid Points Markets, Whales Market. https://app.whales.market/points-markets

Hyperintern, Twitter post. https://twitter.com/Hyperintern/status/1760358830402121947

Brought to you by @DeFiMann and @Ericonomic.

The Alpha Assembly

Receive Telegram notifications of our posts and those of our partners! Join the Alpha Assembly Telegram channel today!

The central hub for everything crypto:

High-level on-chain capital movements

Web3 gaming insights

DeFi research and strategies to give you an edge

Covering everything NFT related: collections, tools, NFT-fi, you name it

News, alpha, and on-the-pulse-content

Thanks for reading, please follow us on Twitter at @Castle__Cap and visit our website to learn more about our services and get in touch.

Virtually yours,

The Castle

In our newsletter, we may discuss projects or tokens in which we hold positions. While we aim to provide informative content, our views are not financial advice. Please conduct your research and consult professionals before making investment decisions. Crypto markets are volatile, and past performance doesn't guarantee future results. Invest responsibly, and be aware of the risks. Your capital is at risk, and we do not accept liability for any losses.

Reply