- The Castle Chronicle

- Posts

- Blurring the Boundaries between DeFi and TradFi: An Introduction to the Real World Assets sector

Blurring the Boundaries between DeFi and TradFi: An Introduction to the Real World Assets sector

⚔️ A Call to Arms

Think you have what it takes to enter the Castle and contribute to research, community initiatives, due diligence analysis, and advising/servicing projects in the space? Or maybe you want to upskill and shadow community members who have already walked a successful path as an intern?

The Evolution of RWAs

The real-world asset (RWA) category has seen substantial growth over the past year.

This has been fueled by two major categories in the space, the tokenization of public securities and private credit, bridging the gap between traditional finance and the digital asset economy.

Higher bond yields have been the main driver in the surge of yield-seeking behavior from retail investors, which have funneled demand into protocols providing this type of product, with one of the primary instruments being US treasuries.

While the tokenization of public securities has brought the vast market of traditional financial assets such as US Treasuries to public blockchains, globalizing their access, private credit projects have served the needs of emerging economies through vehicles to access cheap credit.

Faster settlement times, enhanced transparency, and cheaper operational costs are only some of the value propositions brought by blockchains that are helping accelerate this trend, as the opportunity expands to other financial instruments like equities, private market funds, and real estate.

Over the past year TradFi institutions such as Goldman Sachs, Hamilton Lane, Siemens, and KKR all have announced that they are working towards bringing their RWA on-chain.

On the other hand, decentralized finance (DeFi) protocols such as Maker DAO and Aave are getting ready for it, tailoring their crypto-native platforms to become compatible with RWAs.

For the first time, RWAs allow DeFi the ability to bridge the gap between decentralized financial systems and traditional financial systems. This means DeFi can begin to address the sea of liquidity opportunities and value that exists outside the digital asset space. The traditional financial system is estimated to be worth about ~$600T. If DeFi wants to have a significant impact on how finance is conducted, a successful implementation of RWAs is critical.

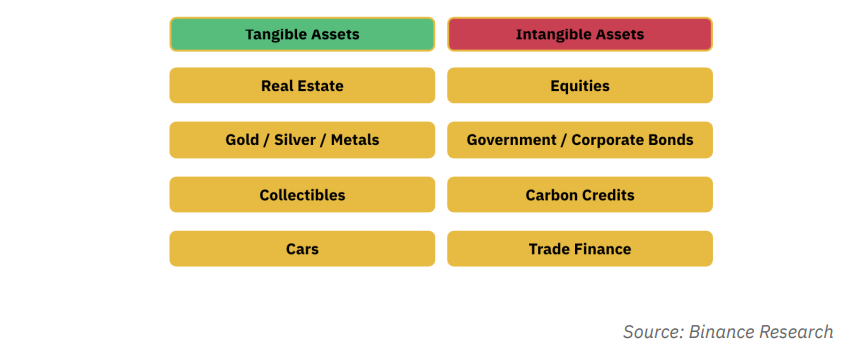

Below is a non-exhaustive list of real-world asset classes that can be brought onto the blockchain through RWAs.

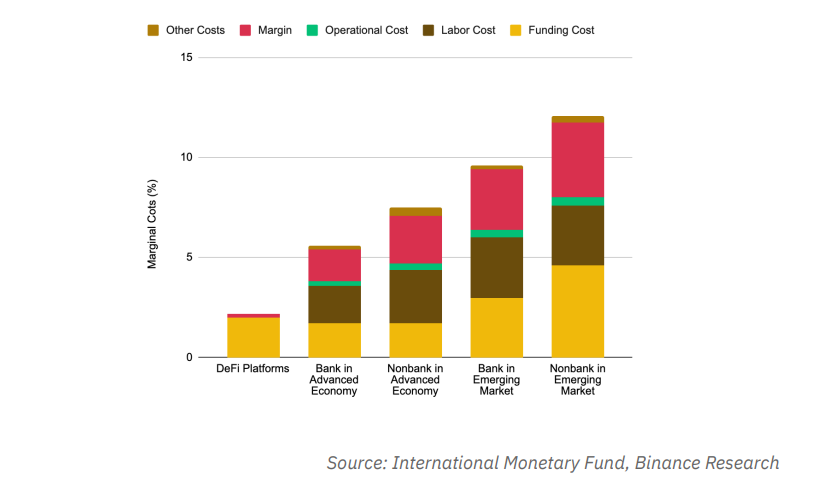

DeFi holds the promise to dismantle some of the constraints found within TradFi, and in turn, deliver material improvements in market efficiency and opportunities for asset holders.

As the name hints, DeFi minimizes or completely cuts out the intermediation systems found in TradFi to effectively decentralize the back end of financial markets. In the International Monetary Fund’s (IMF) 2022 Global Financial Stability Report, the IMF found that DeFi’s nuanced approach to financial markets results in outstanding cost savings as compared to TradFi systems.

Savings mostly accrued from the absence of labor and operational costs, which are normally high in TradFi systems given their complex intermediary systems.

Overall, DeFi has the potential to prove as the superior back-end for financial systems. As the sector continues to mature and prove its viability, asset holders may want to represent their assets via RWAs to access improvements in market efficiency and opportunities brought by DeFi.

Which RWAs Will Drive in More Interest?

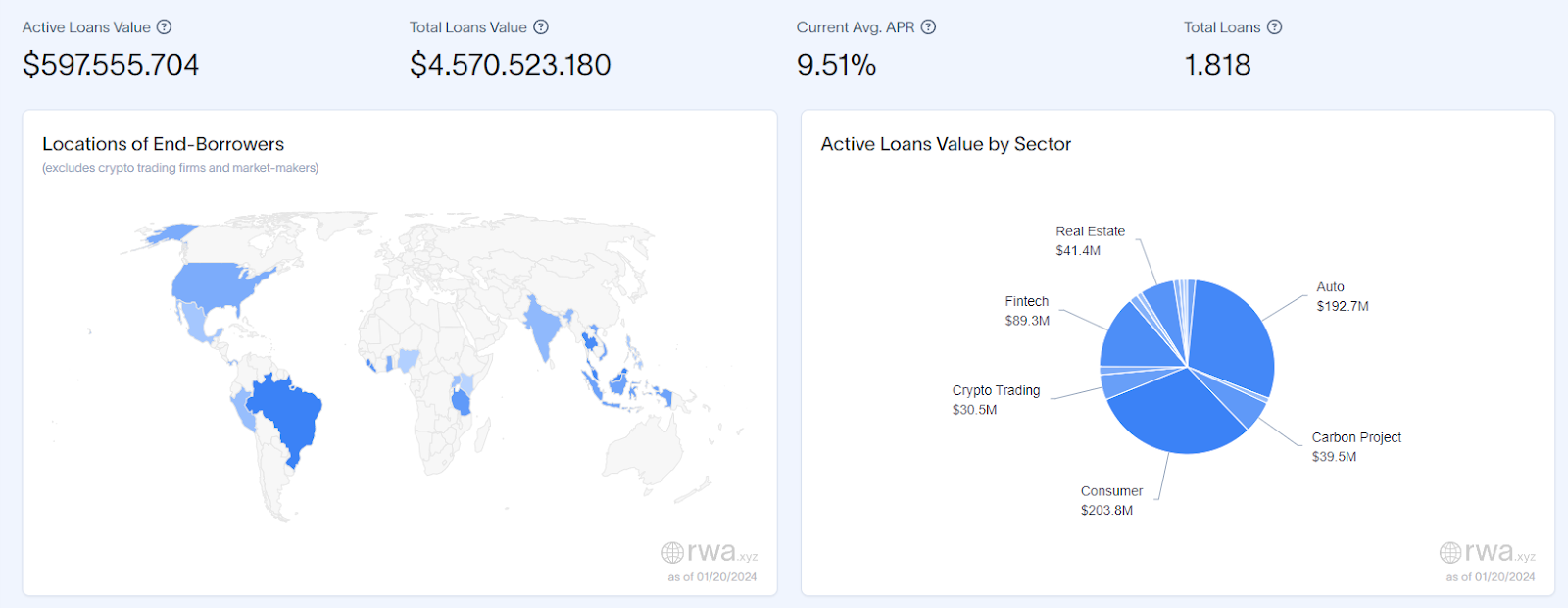

Fixed income is the predominant market in the RWAs space. In comparison to the equity or real asset markets, RWA-based fixed-income markets are more active in terms of transaction flow, rich in terms of offerings, and diverse in terms of market participation. According to RWA.xyz, private credit offerings have comprised over $4.5B in total loan value across 1,560 different loans.

The ability to easily fractionalize and disperse RWAs in DeFi renders previously unfractionalized, total sum, private credit investments accessible to a new set of investors. Borrowers can benefit from private credit-based RWAs because they can reach a new market of lenders through fractionalization and the lowering of liquidity barriers. DeFi investors are able to gain exposure to private credit markets which, in the TradFi space, have been traditionally reserved for credit funds and other institutions with access to large sums of capital and private connections.

Additionally, a bright spot within the RWA space in recent months has been tokenized U.S. Treasuries, which refer to sovereign debt issued by the U.S. government and have been widely considered a benchmark for risk-free assets in traditional financial markets. Against the backdrop of rising interest rates, treasury yields have steadily inched higher and now comfortably exceed DeFi yields.

Demonstrating the utility of RWAs, investors today can take advantage of real-world yields by investing in tokenized treasuries without leaving the blockchain. The tokenized treasury market is worth more than $600M, meaning that investors are effectively lending that amount to the U.S. government at around 4.2% APY.

RWA for Institutional Investors

Below is a short overview of actions taken by significant institutions worldwide regarding tokenization and adoption of DeFi.

JP Morgan - Launched their private blockchain and is positive about the tokenization of multiple types of assets.

BlackRock - Experimenting with tokenization of money market fund shares on JP Morgan’s blockchain.

PayPal - First major U.S. institution to launch a stablecoin.

Franklin Templeton - Launched an on-chain Money Fund on Polygon and invested in different Web3 startups.

Deutsche Bank - Investing and working with startups to establish digital asset custody and tokenization services.

BBVA - Became the first global bank to offer crypto asset custody services in Spain.

UBS - Launched its blockchain platform to provide asset management services and introduced a digital bond that is publicly traded and settled on both blockchain-based and traditional exchanges.

Santander - Banco Santander announced a few years ago that it had issued the first end-to-end blockchain bond. The bank issued the bond directly onto the blockchain, a first step towards a potential secondary market for mainstream security tokens in the future.

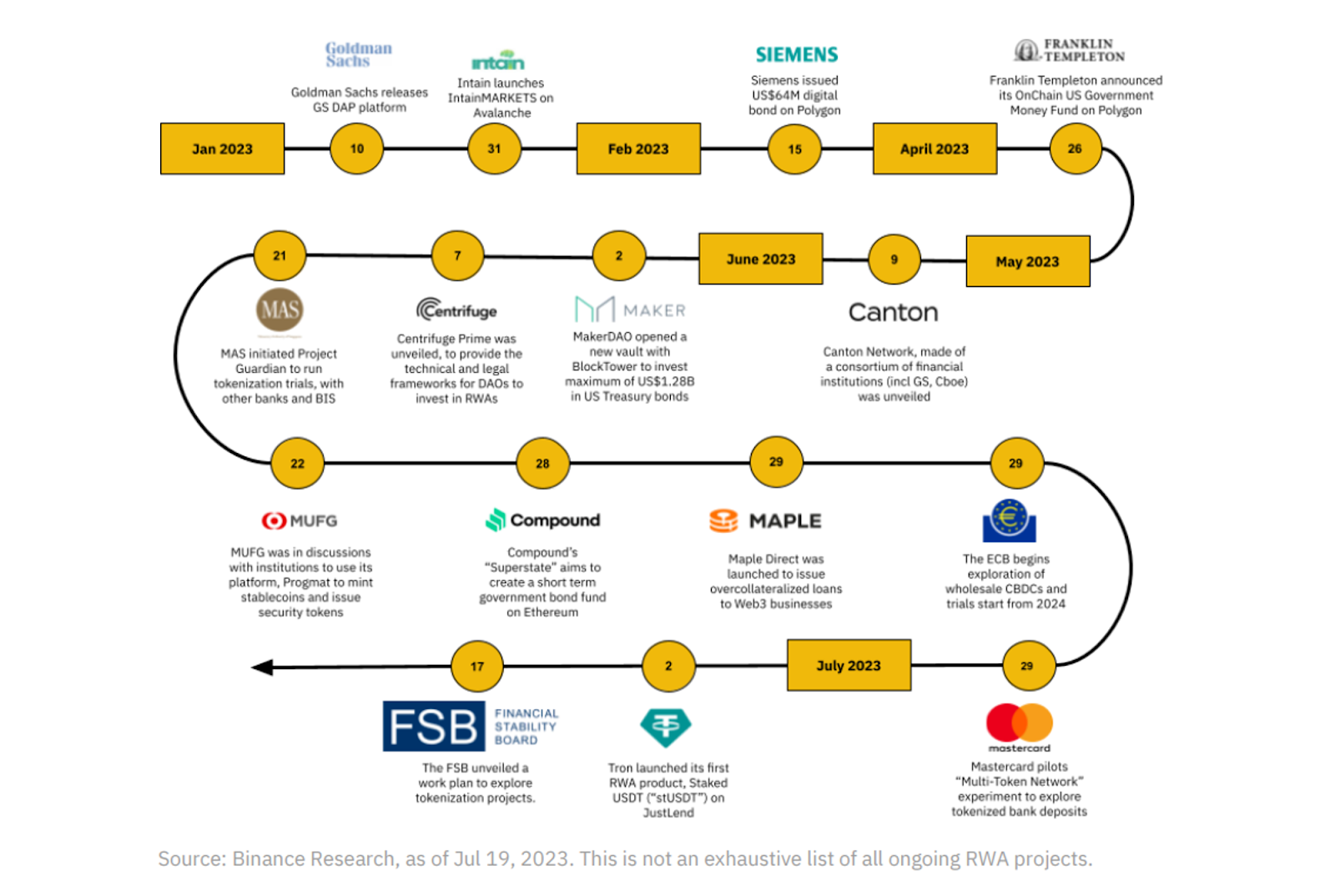

This infographic shows how adoption of these technologies by institutional investors has grown within the last 12 months.

Project Guardian

Among the many cases of increased institutional adoption of blockchain-based technologies, Project Guardian is likely the most relevant and advanced case to look at.

Project Guardian is a collaborative initiative led by the Monetary Authority of Singapore (MAS) bringing multiple industries together through various pilots to explore how to integrate digital assets into the traditional financial system, ultimately enhancing the overall efficiency, accessibility, and security of financial transactions.

The MASis one of the world’s leading Asian fintech hubs, delving into the potential for Web3 and the future of DeFi as an emerging technology.

Project Guardian serves as a testbed for financial institutions and FinTech companies to experiment with and learn about the application of blockchain and DeFi technologies in a controlled environment.

MAS has already paved the way with a pilot event that marked a significant milestone in DeFi. This event saw heavyweights like JP Morgan and SBI Digital Asset Holdings engaging in foreign exchange and government bond transactions against tokenized liquidity pools, setting a new precedent in the financial industry.

The highlight of this pilot was a live currency transaction, a first of its kind, involving tokenized Japanese Yen (JPY) and Singapore Dollar (SGD) deposits. Furthermore, the event included a highly intricate simulation exercise involving buying and selling tokenized government bonds.

Project Guardian is innovating in DeFi and tokenization and pioneering the concept of Trust Anchors in the DeFi space. These anchors are essentially regulated financial institutions, meticulously selected and tasked with a critical role: screening, verifying, and issuing verifiable credentials to entities wishing to participate in DeFi protocols.

This approach brings a new level of integrity and security to the DeFi ecosystem, thus ensuring that all participants, whether traders, issuers, or protocol developers, are thoroughly vetted and verified. With this system, the risks typically associated with anonymous or unverified interactions in the DeFi space are mitigated.

For institutional players, the introduction of Trust Guardians is a game-changer, as it addresses one of the primary concerns hindering broader institutional adoption of DeFi and tokenization: security and trust.

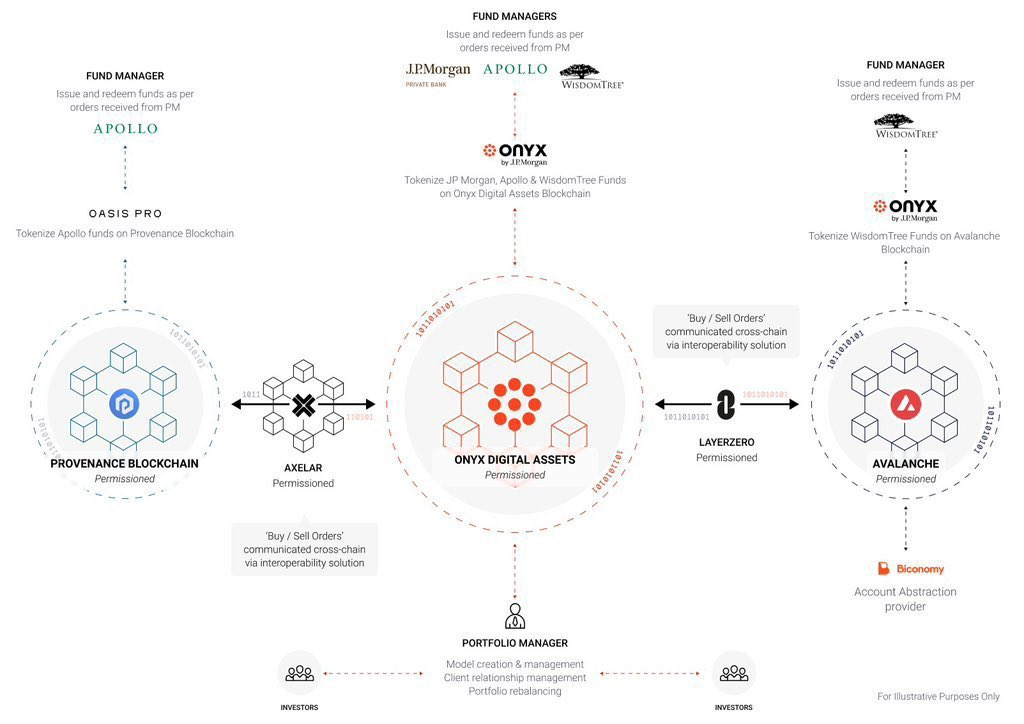

RWAs in a Cross-chain World

Along with being secure when engaging with verified counterparties, institutions aim to not worry about which chain they're working on, as they will be utilizing interoperability solutions to easily communicate from one chain to another.

Banks, asset managers, and other entities want to have the possibility to move money anywhere they need.

An example of this is shown by this infographic where Axelar Network and Layerzero are used as "bridges" to let all networks communicate with each other.

These protocols act as the key connectors, effectively breaking down the communication silos that have traditionally existed between various blockchain networks, having a strong impact on:.

Asset and Information Mobility: Interoperability protocols enable the free flow of digital assets and essential information across diverse blockchain ecosystems.

Enhanced Developer Flexibility: By leveraging these protocols, developers are equipped to craft applications that draw from the strengths of multiple blockchains, hopefully leading the way to more optimized and robust decentralized solutions.

Interoperability protocols act as blockchain abstraction layers. Such layers play a pivotal role in streamlining cross-chain communication, allowing both traditional systems and decentralized applications (dApps) to interact with any blockchain through a single unified protocol. Without these tools, the integration process of RWA would be much more complex, needing unique configurations for each chain interaction (heavily fragmenting the overall UX).

Currently, in DeFi, three interoperability solutions come on top of others:

CCIP

Layerzero

Axelar Network

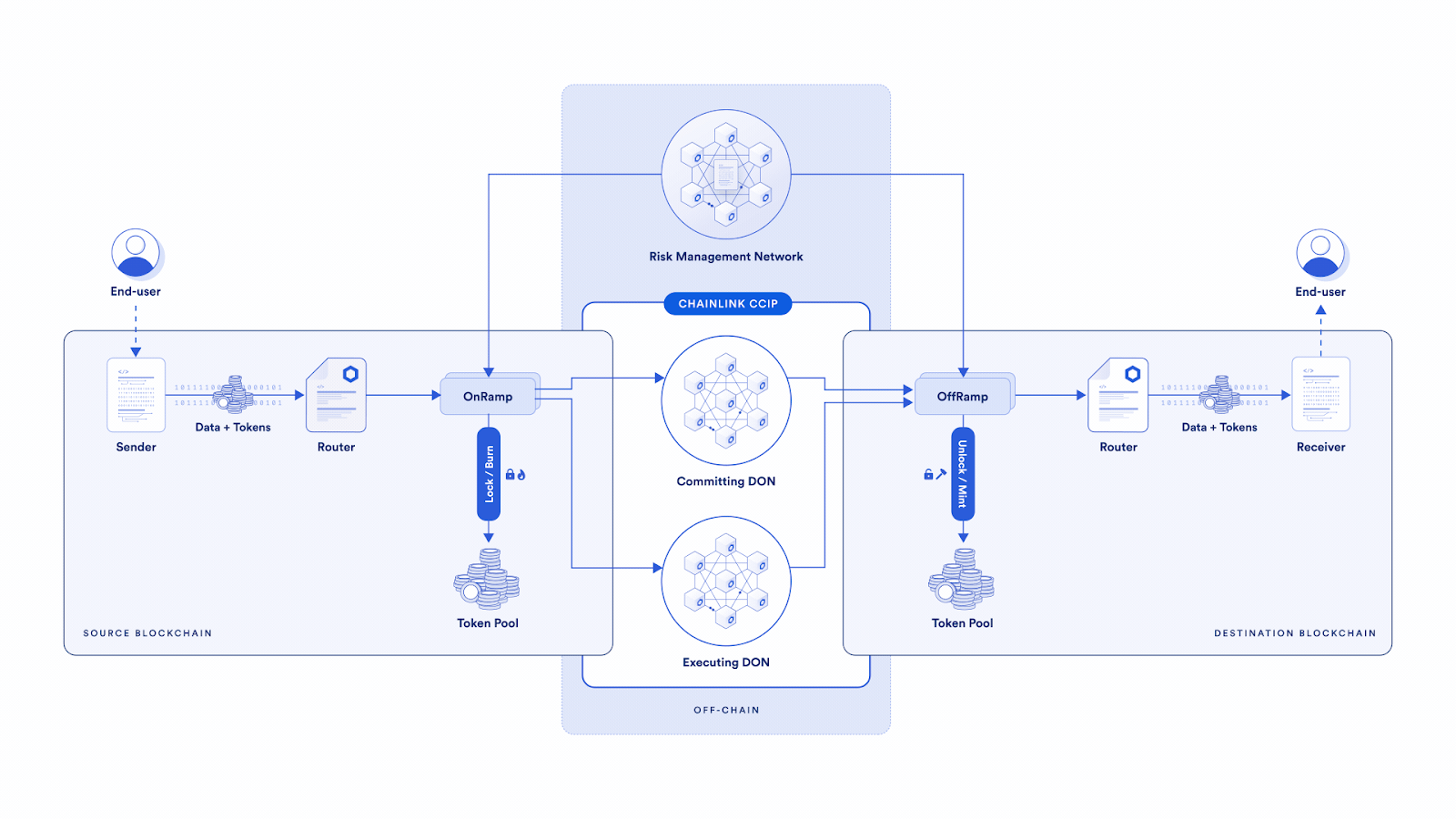

CCIP by Chainlink

CCIP enables a sender on a source blockchain to send a message to a receiver on a destination blockchain.

The system is based on 5 on-chain components:

Router

Decentralized Oracle Network (DON)

Risk Management Network

On/Off Ramp System

Token Pool

Router

The Router is the primary contract CCIP users interface with, and it's responsible for initiating cross-chain interactions and "delivering" the tokens to users.

There is a Router on each supported blockchain.

Decentralized Oracle Network (DON)

CCIP supports two DONs: The Committing DON and the Executing DON.

The first one is responsible for monitoring the on-ramp, bundling transactions, and storing them in the "commitStore contract" while the second executes the transactions.

Having separate commitment and execution permits the Risk Management Network to have enough time to check the commitment of messages before executing them.

This system constantly ensures the integrity of the committed Merkle roots (series of transactions) by DONs.

Risk Management Network

The Risk Management Network is built using off-chain and on-chain components:

Off-chain: Several Risk Management nodes continually monitor all supported chains against abnormal activities

On-chain: One Risk Management contract per supported CCIP chain

The Risk Management Network is a secondary validation service parallel to the CCIP system. It doesn't run the same codebase as the DON to mitigate the risk of vulnerabilities that might affect the DON's codebase.

On/Off Ramp System

On-ramp system: It verifies size, gas limit, validity of transactions, and order of messages and other tasks.

Off-ramp system: It verifies the proofs given by the Executing DON and makes sure transactions are only executed once.

Token Pool

Finally, each token has its token pool to facilitate On-Ramp and Off-Ramp operations. Token pools are configurable to lock or burn at the source blockchain and unlock or mint at the destination blockchain.

To summarize, with the CCIP, tokens do not physically move across chains. Instead, they are locked or burned on one chain and then unlocked or minted on another. The most important components of this model are the two DONs (Oracle networks) and the Risk Management network.

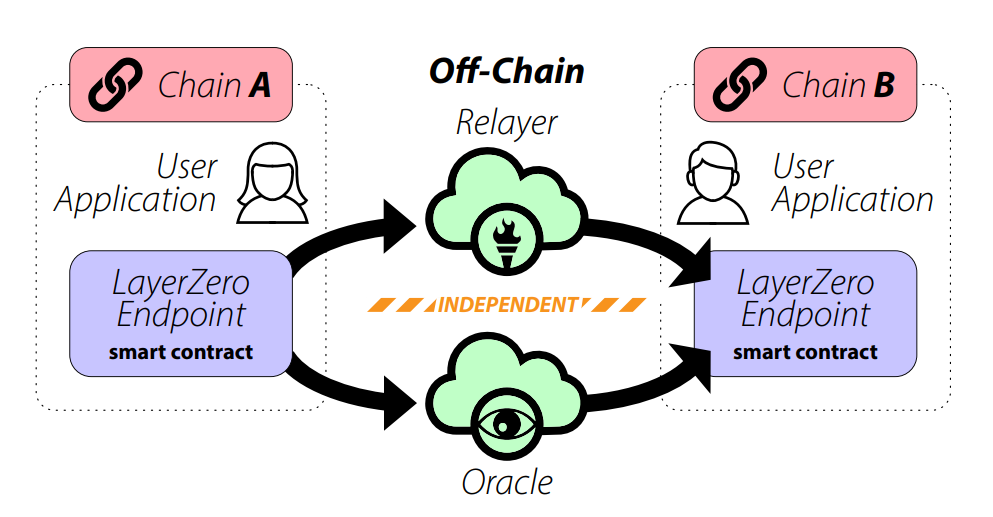

LayerZero

LayerZero conveys information between two on-chain endpoints by running (Ultra) Light Nodes and utilizing relayers and decentralized oracles. Data conveyed in this process range from plain data to state changes and high-level communications between decentralized networks.

Ultra Light Nodes keep proof of every transaction on the source chain and provide them in bulk whenever the destination chain requires them. These nodes account for security and cost-effectiveness while oracles and relayers in synergy power the data transfer system.

The system is based on 3 on-chain components:

Ultra Light Nodes

Oracles

Relayers

Ultra Light Nodes

Light Nodes are comparable to mini validator nodes on a blockchain network. For interoperability protocols, the Light Nodes are set up on the destination chain. As described earlier, Light Nodes foresee the reception of data from a source chain and the subsequent integration of the conveyed data into the destination chain, completing the communication cycle.

In doing so, Light Nodes sacrifice cost-effectiveness for improved security. As a fix, LayerZero uses Ultra Light Nodes (ULNs). ULNs are very much like Light Nodes, but instead of sequentially adding each new transaction to the destination chain, Ultra Light Nodes package these transactions and send them all at once at the request of the destination chain. LayerZero claims that this process saves cost while maintaining the level of security offered by on-chain Light Nodes.

Oracles

Oracles are relational database management systems. Blockchain oracles enable decentralized systems to communicate with the world outside of it. Oracles generate data feeds and integrate them into the “target system” in a format that facilitates its utilization. LayerZero interoperability protocol uses decentralized oracles like the ones developed by Chainlink and Band protocol.

Relayers

Relayers complete a messaging cycle between communicating networks by sending proof of transaction to the destination. With the proof, the destination chain can integrate the data or message from the source chain into its system and execute possible commands from the message.

How Does LayerZero Work?

LayerZero creates endpoints on each of the communicating networks, Network A (source chain) and Network B (destination chain).

To send a message to Network B, a user application from Network A selects a preferred oracle and a relayer for their cross-chain message.

The endpoint at Network A feeds the oracle and the selected relayer with the details of the message including its destination.

The oracle forwards the details of this message to Network B while the relayer submits proof of the transaction to the target chain.

The communication between the oracles and the target chain takes the same form as when oracles feed blockchain protocols with data from the external environment.

CCIP vs Layerzero

CCIP is quite similar to LayerZero. Instead of having a DON (decentralized oracle network) and a relayer the CCIP uses two DONs (committing DON and executing DON).

Additionally, CCIP has an added security layer in the form of Active Risk Management network.

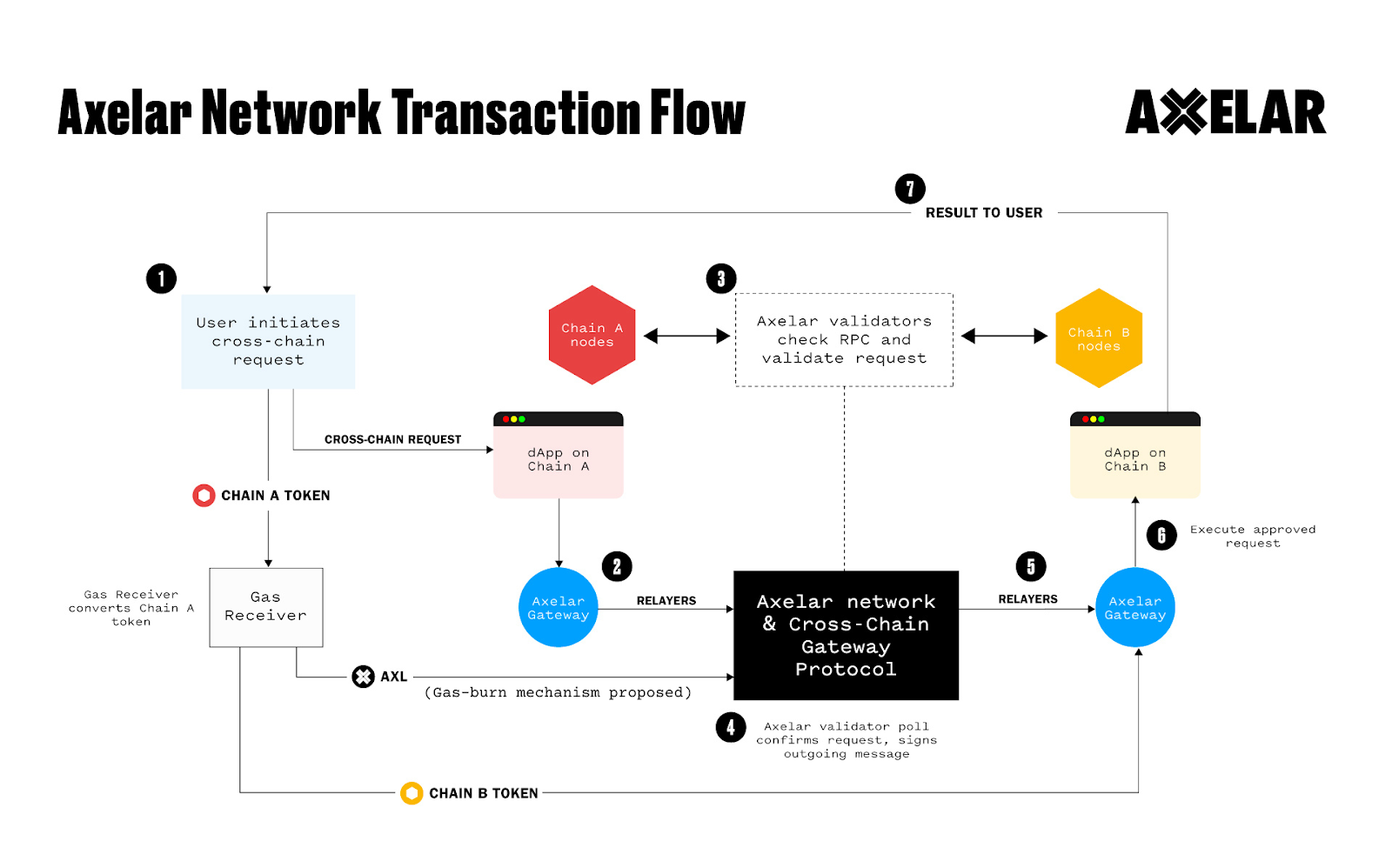

Axelar Network

The Axelar network is a blockchain that connects blockchains, enabling universal Web3 interoperability. The network is secured using proof-of-stake consensus, and messages are routed and translated using permissionless protocols.

Axelar comprises a decentralized network of validators, secure gateway contracts, uniform translation, routing architecture, and a suite of software development kits (SDKs) and application programming interfaces (APIs) to enable composability between blockchains.

The Axelar network has three key components across two functional layers.

A Decentralized Network

The first is the decentralized network itself, supported by a set of validators that are responsible for maintaining the network and executing transactions.

The validators run the cross-chain gateway protocol, which is a multi-party cryptography overlay that sits on top of Layer 1 blockchains. They are responsible for performing read and write operations to gateway smart contracts deployed on external connected chains, voting and attesting to events on those chains.

Gateway Smart Contracts

The second component is the gateways — smart contracts that provide the connectivity between Axelar network and its interconnected Layer 1 blockchains:

Validators monitor gateways for incoming transactions, which the validators READ.

They then come to a consensus on the validity of that transaction

Once agreed, they WRITE to the destination chain’s gateway to execute the cross-chain transaction.

The validators and gateways compose the core infrastructure layer.

Developer Tools

The APIs and SDKs (the libraries and tools that enable developers to access the Axelar network easily) sit on top of the validators and gateways. This is the application-development layer that developers will use to compose across any two chains in a single hop, adding universal interoperability to their blockchains and applications.

Using Axelar, they can lock, unlock, and transfer assets between any two addresses on any two blockchain platforms, execute cross-chain application triggers, and more generally handle any cross-chain requests.

How Does Axelar Work?

A dApp user initiates a cross-chain message via the Axelar Gateway on the source chain. This action triggers an event, which is then propagated by a relayer to Axelar's validators for processing.

Validators verify the event’s authenticity by confirming that their nodes on the source chain have observed it.

Once validated, a requisite number of validators who hold a share of cryptographic keys must authorize the message.

Following authorization, the message is relayed to the destination chain, where it is ready for execution.

Overview of RWAs Protocols

Now that we've identified the protocols taking the lead in enabling interoperability for RWA, it's time to examine the main RWA projects within this sector.

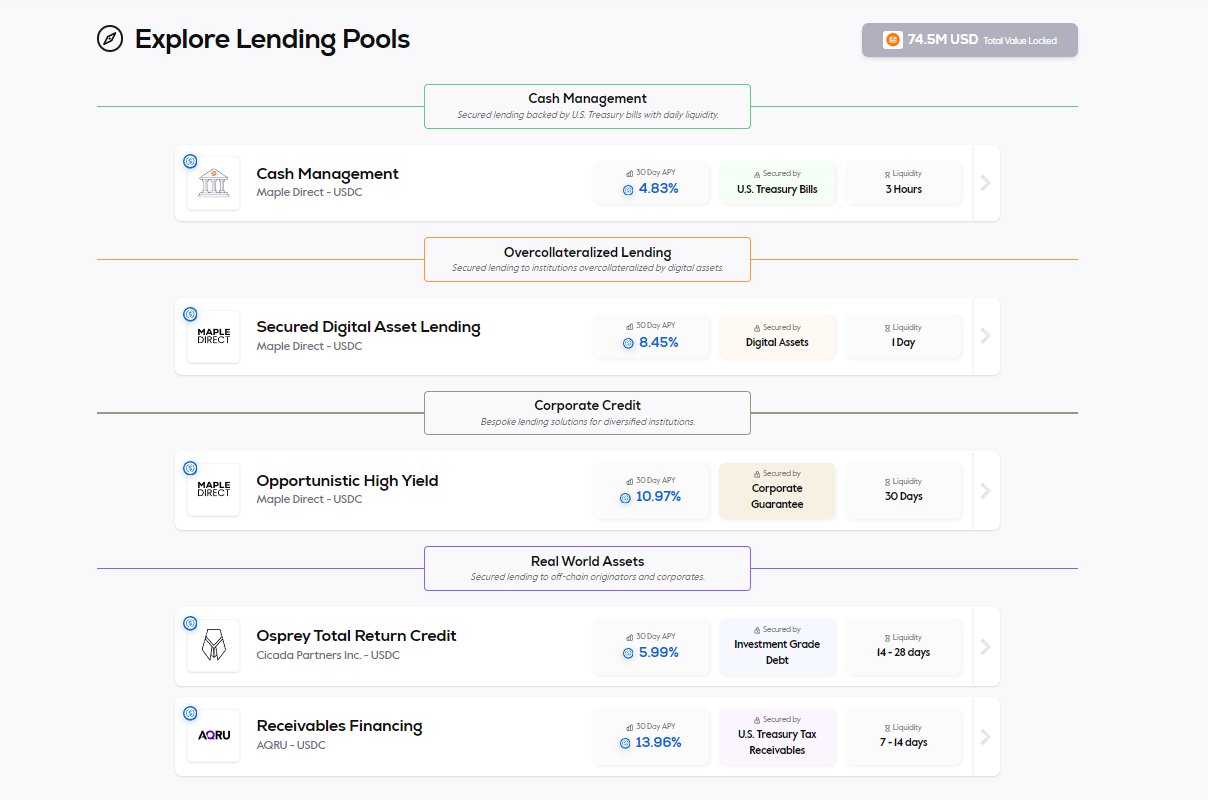

Maple Finance

Maple Finance is an institutional capital network that provides the infrastructure for credit experts to run on-chain lending businesses and connects institutional lenders and borrowers. Maple Finance has three key stakeholders: borrowers, lenders, and pool delegates.

Institutional borrowers can access financing options on Maple Finance.

Lenders can obtain a yield on their assets by lending to borrowers.

Pool delegates are credit professionals who assess, manage, and underwrite loans.

Today, Maple Finance is one of the market leaders in the private credit space, with more than $332M in outstanding loans

Capitalizing on the increasing demand for treasuries, Maple rolled out a U.S. Treasury pool in April, allowing non-U.S.-accredited investors and entities to access U.S. Treasury bills directly. The pool is backed by U.S. Treasury bills and reverse repurchase agreements, targeting a net APY of the current one-month U.S. Treasury bill rate minus fees and expenses of 1.0% annualized. This essentially serves as a cash management solution for stablecoin holders to earn yield.

Reserve Protocol

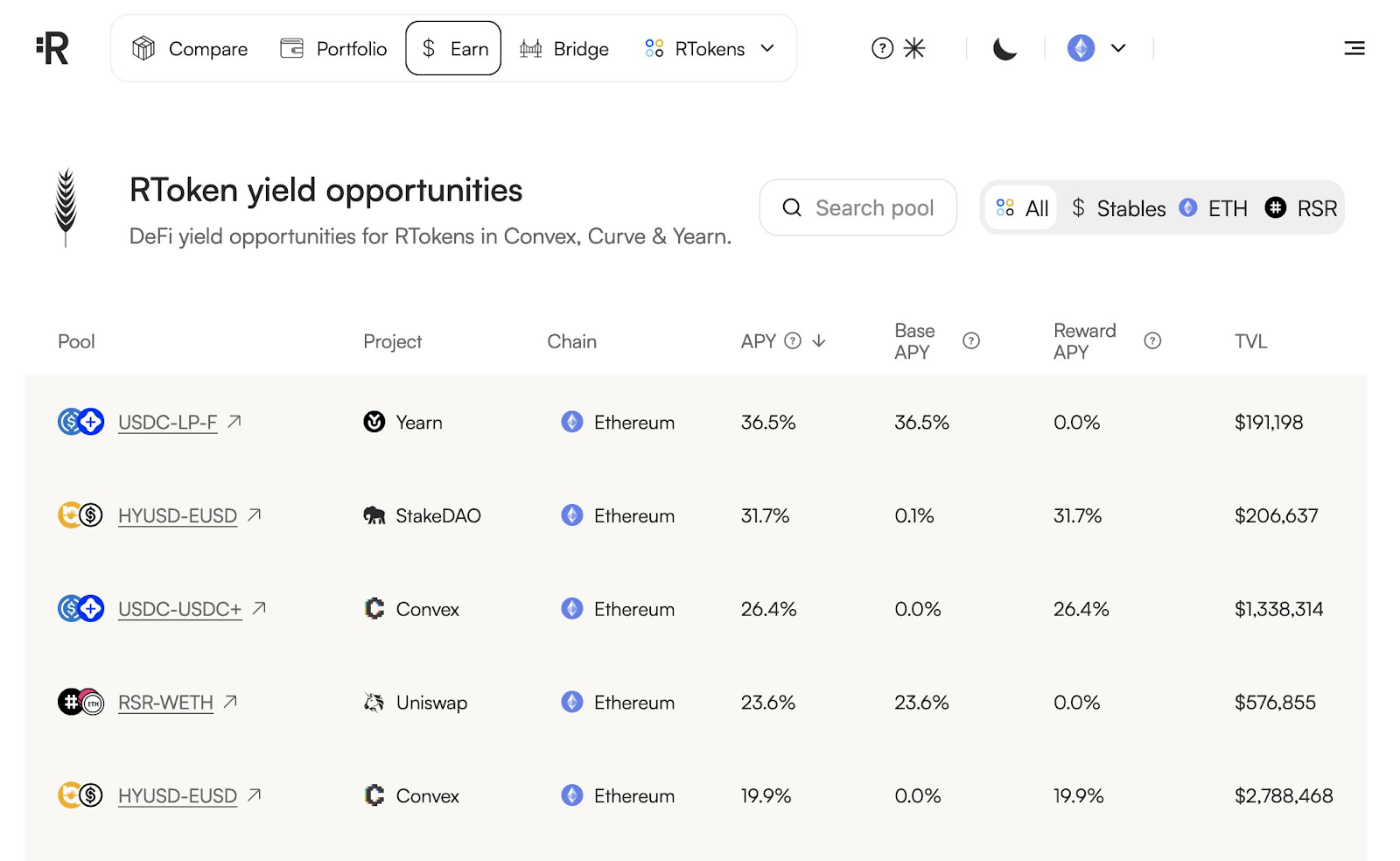

Reserve Protocol allows anyone to create stablecoins backed by baskets of ERC-20 tokens on Ethereum and Base. Stable asset-backed currencies launched on the Reserve protocol are called “RTokens”.

Once an RToken configuration has been deployed, RTokens can be minted by depositing the entire basket of collateral backing tokens and redeemed for the entire basket as well. Thus, an RToken will tend to trade at the market value of the entire basket that backs it, as any lower or higher price could be arbitraged.

Each RToken is governed separately, and each can have an entirely different governance system. Furthermore, RTokens can generate revenue, and this revenue is used to incentivize RSR holders to stake. Revenue can come from yield from lending collateral tokens on-chain or revenue shares with collateral token issuers. Governance can also direct any portion of revenue to RSR stakers, to incentivize RSR holders to stake and provide over-collateralization.

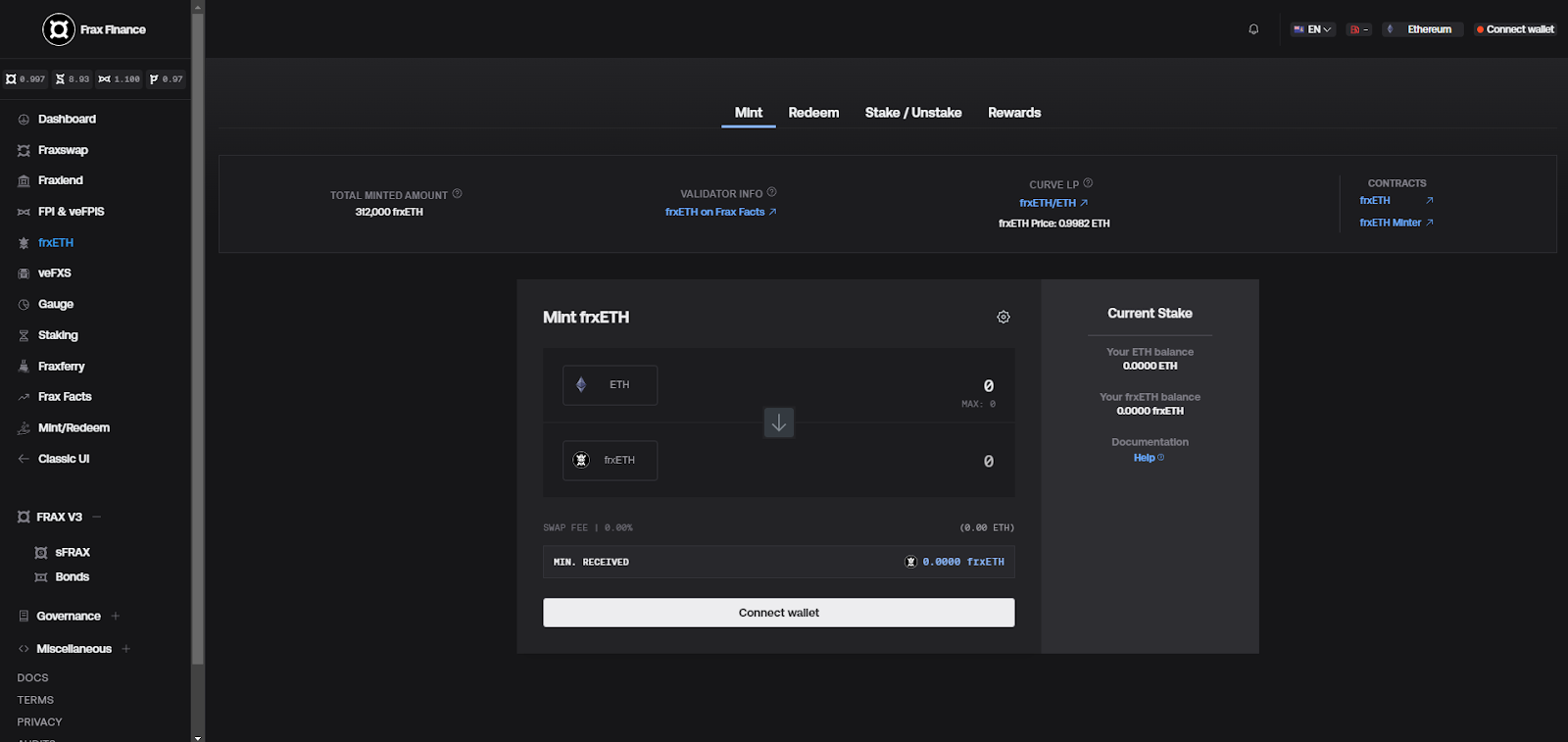

Frax Finance

Frax Finance is a versatile DeFi protocol that encompasses a suite of DeFi products, including its native stablecoin FRAX, a liquid staking solution with frxETH, and an array of other financial instruments. The platform has positioned itself as a multifaceted player in the decentralized finance landscape.

Frax Finance’s operation centers around several core components:

$FRAX Stablecoin: The main product of Frax Finance, $FRAX, is a stablecoin that initially drew from both collateralized and algorithmic stablecoin designs. The protocol has since transitioned to a fully collateralized model, aiming for a 100% collateralization ratio.

Minting and Redemption Mechanism: Users can mint $FRAX using less than $1 of collateral combined with $FXS tokens when its price is above $1, providing an arbitrage opportunity. Conversely, when the price is below $1, users can redeem $FRAX for an equivalent amount of collateral and $FXS tokens.

Expansion of Services: Beyond the $FRAX stablecoin, the protocol includes a lending platform, an Automated Market Maker (AMM), an inflation-linked stablecoin ($FPI), and liquid staking represented by the $frxETH token.

Governance Token ($FXS): $FXS serves as the governance token within the Frax Finance ecosystem, allowing holders to participate in decision-making and governance processes.

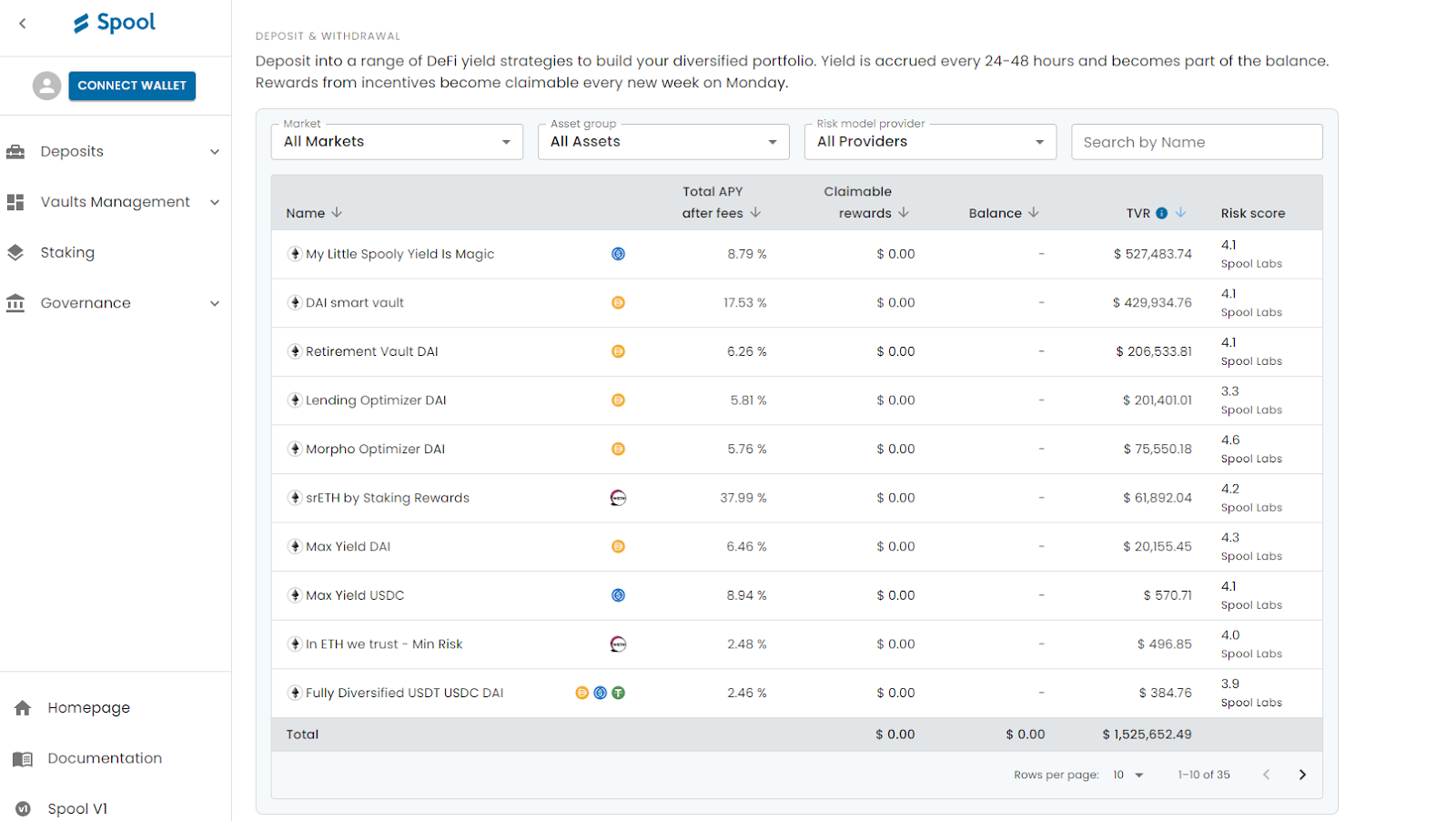

Spool

Spool is an infrastructure protocol providing yield opportunities to DeFi users and institutional investors.

The protocol acts as DeFi middleware routing all funds in the protocols selected by the user to generate passive yield.

Spool offers a way to participate in multiple yield generation methods while maintaining adequate diversification, managing risk appetite, and benefiting from economies of scale when it comes to rebalancing and compounding. A user simply deposits into an existing Spool Smart Vault (or makes its own) and in turn, enjoys automated and optimized decision-making curated by the Spool DAO.

Spool is DeFi middleware, which connects users to existing and new Yield Generators & Yield Optimizers. In doing so, it routes TVL to existing DeFi Protocols while maintaining freedom & flexibility for its users.

Good middleware is unnoticeable and Spool operates in the background to the benefit of all participants within the ecosystem. Spool Smart Vaults can be seamlessly integrated into UIs via the SDK, allowing professional users like businesses to create white-labeled DeFi products for end-users.

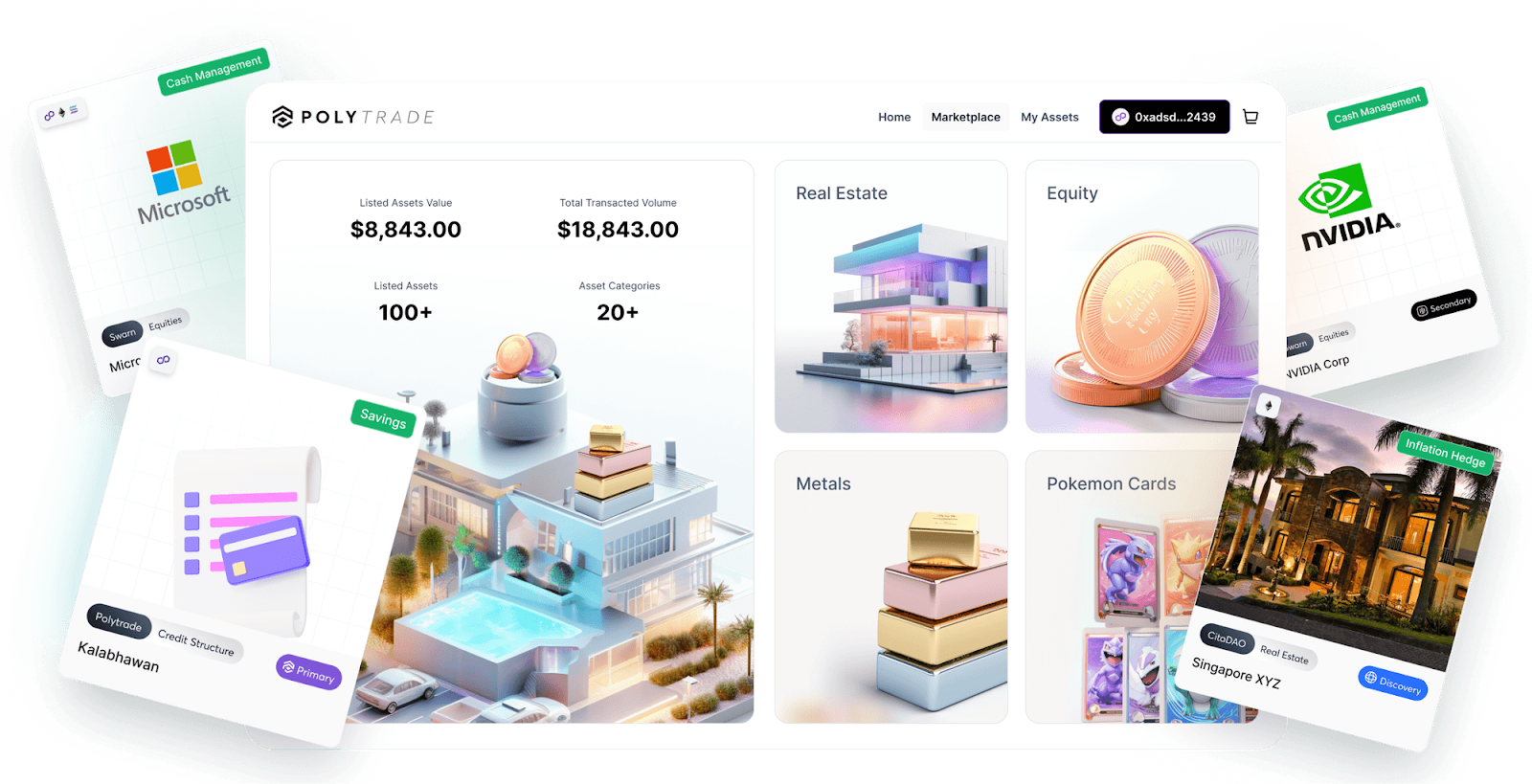

Polytrade

Polytrade is a Polygon-based marketplace for buying, selling, and managing RWAs in addition to fractionalizing assets and trading parts of them.

The protocol tokenizes assets and assigns them to each lending pool on its Lender Portal. The Proof of Trade mechanism ensures transparency by mapping the underlying collateral via NFTs, which helps users easily view the assets associated with each pool on the Polytrade website.

The asset originator will burn and settle all tokens at maturity while Polytrade ensures that the assets are held with the originator and are incorporated with appropriate legal documentation. This way, the platform aims to gate the marketplace to only allow quality assets.

Parcl

Parcl is a perpetuals dex that offers real estate index markets for speculation or hedging. Core features and improvements on previous iterations include more scalable liquidity provision, flexible governance, and risk management features that protect LPs and traders from excessive market imbalance. The design is heavily influenced by Synthetix perps.

The protocol can support many exchanges where each exchange has a single collateral and a single LP pool.

Markets on Parcl belong to a single exchange. Each market's counterparty for trading is its associated exchange's LP pool. LPs underwrite and clear all trades, collect the majority of trading fees that they split with the protocol and act as that particular exchange's insurance fund. It is as if the LP pool has a monopoly market-making privilege on that exchange's markets.

The protocol's risk management features promote a delta-neutral LP experience by creating incentives to decrease market skew and levying penalties on traders who increase market skew.

If risk management parameters happen to be insufficient, then governance will adjust them and fine tune them over time.

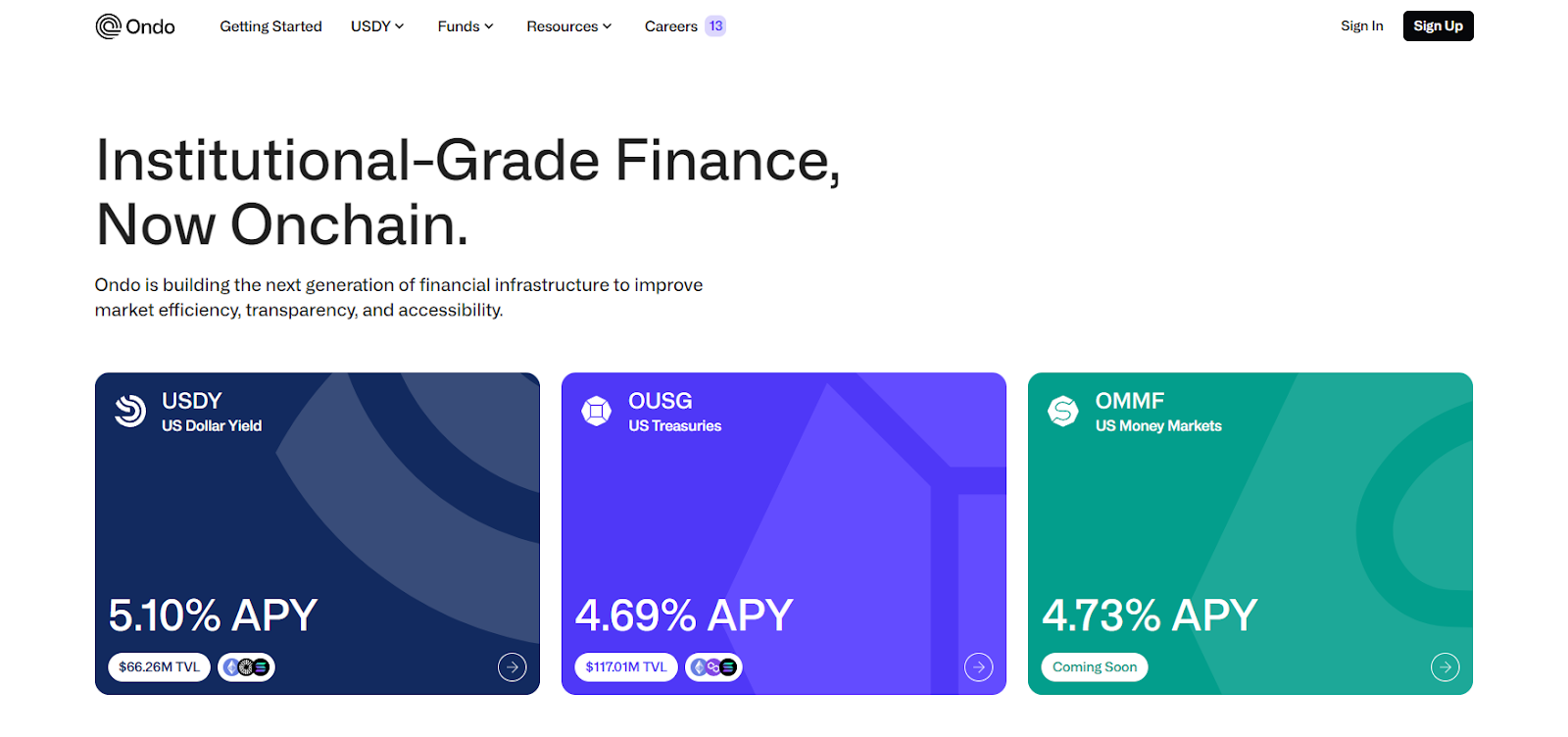

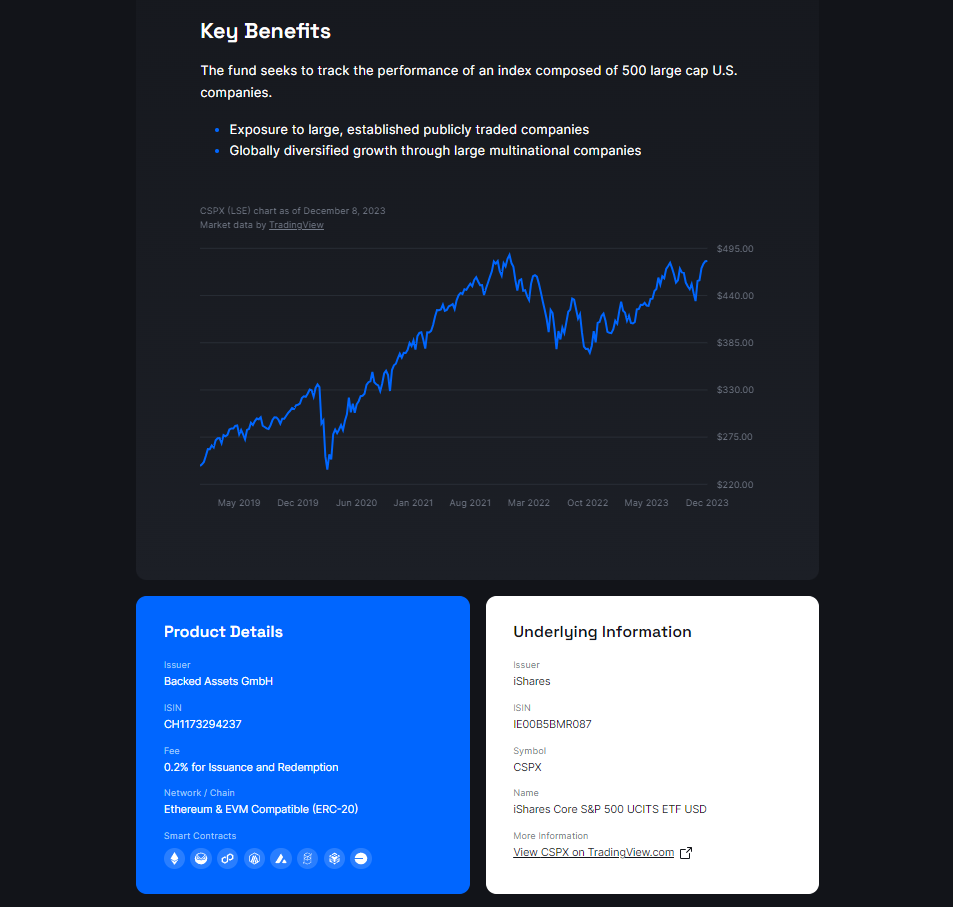

Ondo Finance

Ondo Finance provides institutional-grade, blockchain-based investment products and services. The firm is led by a former Goldman Sachs employee and is backed by notable investors including Coinbase Ventures and Tiger Global.

Ondo has four RWA offerings, providing investors access to a range of cash management products and bond funds. In terms of the process, an investor can deposit USDC, which is exchanged for USD, to purchase assets such as ETFs or funds. In return, new fund tokens are minted and deposited into the investor’s wallet. At the point of redemption, tokens are burned, and USDC is returned.

Ondo offers four different RWA options to investors:

U.S. Money Markets

Short-Term U.S. Government Bond Fund

Short-Term Investment Grade Bond Fund

High Yield Corporate Debt

Ondo Finance has a 25% market share within the tokenized treasury space.

MakerDAO

MakerDAO has been the top accumulator of RWAs with $2.5bn worth of RWAs under its treasury.

Maker allows users to deposit collateral into their vaults and take out $DAI-denominated debt in return. The collateral supported includes $ETH, stablecoins, wrapped $BTC, liquid staking derivatives (“LSDs”), and others.

Maker also offers $DAI loans in return for RWA collateral for borrowers that have been whitelisted through MakerDAO. Borrowers include Huntingdon Valley Bank, which has a US$100M RWA-collateralized loan vault with Maker.

RWAs now represent over 49% of assets on Maker’s balance sheet. A significant portion of these RWAs are U.S. Treasury bills, which have benefited from the rising interest rate environment and seen high yields in the last 18 months or so. This has meant that RWAs currently make up over 60% of Maker’s revenue, which itself breached all-time highs at over $200M (annualized) earlier in November.

RWAs and, specifically, U.S. Treasuries will likely continue to play a significant role in MakerDAO’s balance sheet, at least in the foreseeable future.

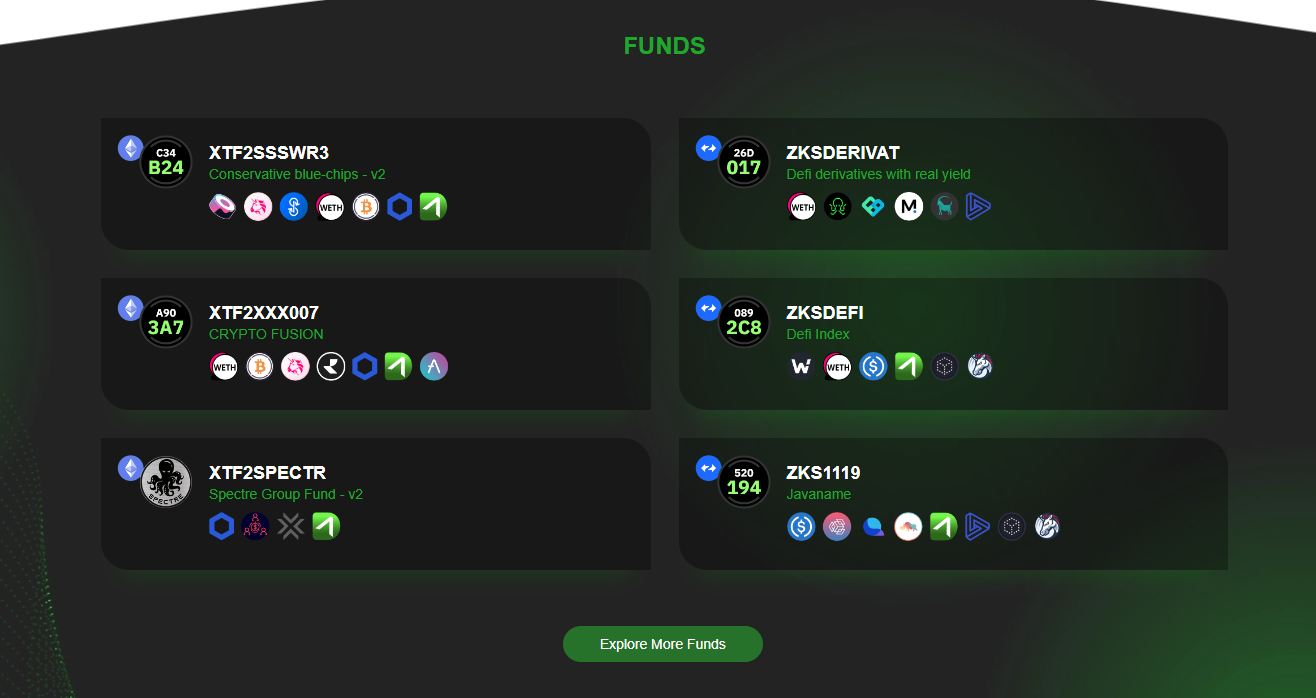

Domani Protocol

DOMANI is an asset management protocol that empowers anyone to mint, trade, redeem, and provide liquidity on non-custodial oracle-less tokenized portfolios (XTFs). These XTF tokens are unique for each fund created, and users can earn rewards and fees by providing liquidity.

The platform is deployed on Ethereum, zkSync, and Avalanche with more than 150+ active funds created by the community members.

The DOMANI protocol can be upgraded and configured by token holders and their delegates. All potential changes to the protocol, including the adjustment of system parameters like management fee factors or interest rate algorithms, must pass through a proposal and voting process as specified in the governance smart contracts.

Last year DOMANI announced a partnership with Deutsche Bank to experiment with digital fund management and investment servicing.

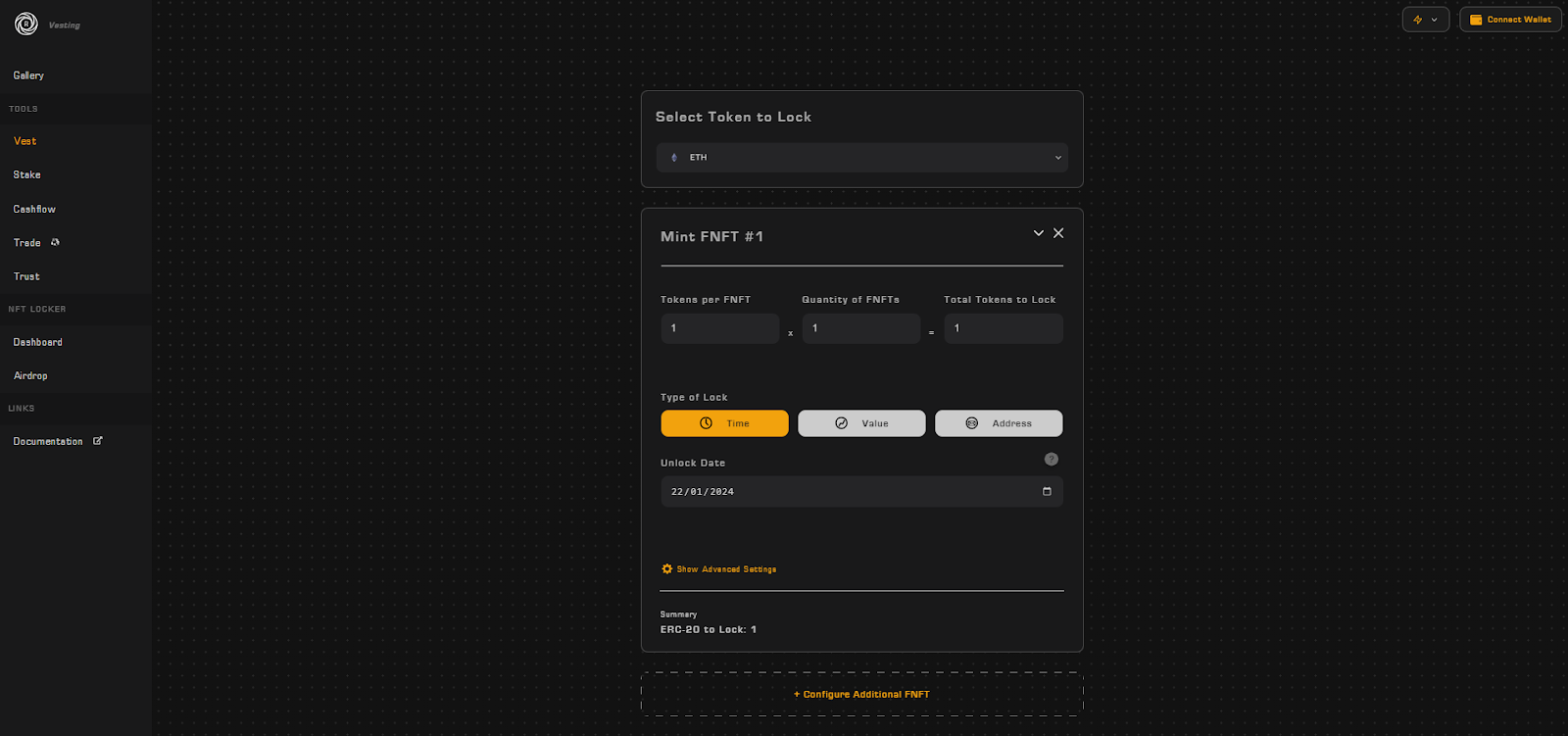

Revest Finance

Revest proposes a new protocol for packaging, transferring, and storing of fungible ERC-20 tokens as non-fungible tokenized financial instruments, leveraging the ERC-1155 Non-Fungible Token (NFT) standard for ease of access and universality of commerce.

FNFTs, the NFTs model introduced by Revest, are created when a set amount of ERC-20 tokens is deposited into a Revest Smart Vault.

The newly created Smart Vault only returns the underlying tokens to actors who satisfy the following two conditions:

Possession of the FNFT itself

One of the three possible locking mechanisms (Time, Value, or Address) placed on the vault at creation has unlocked

For the underlying value to be retrieved from the Smart Vault, the FNFT representing part of that underlying must be burned and the locking mechanism on the Smart Vault must be satisfied.

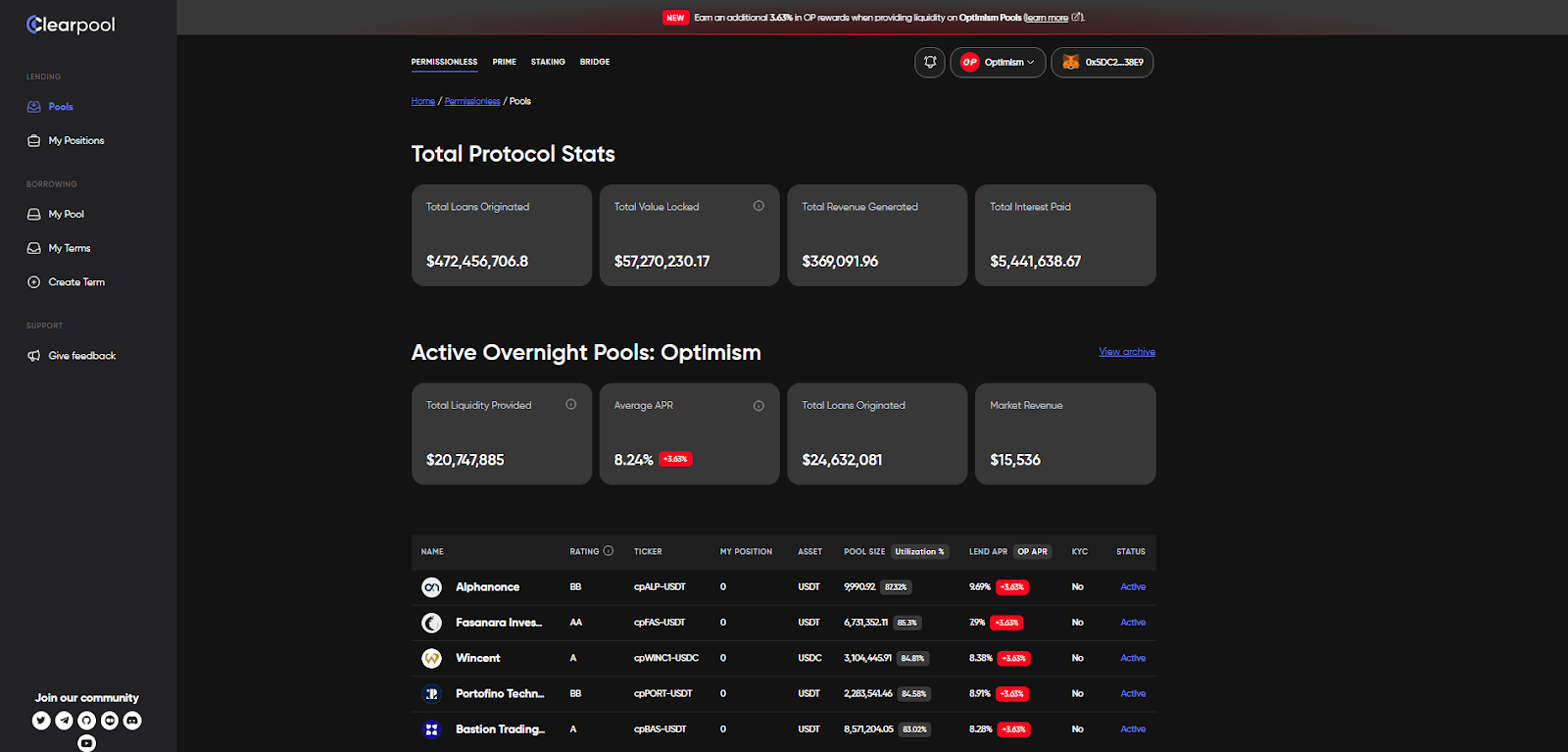

Clearpool

Clearpool is a decentralized marketplace allowing institutions to borrow funds from a decentralized network of lenders without the need for collateral.

The platform offers a permissionless solution for DeFi individuals and a KYC & AML-compliant solution for institutional investors. This way, the project “democratizes” the credit market, which has traditionally been closed to retail investors, and gives institutional borrowers direct access to a diversified and decentralized network of lenders.

Borrowers, typically institutions, can access unsecured liquidity, and eliminate risks of liquidation, significantly enhancing capital efficiency.

Lenders (liquidity providers/LPs), typically individual or institutional investors, are rewarded fairly for risk-taking, with pool interest rates rising when risk increases, and falling when risk decreases.

BackedFi

BackedFi allows users to invest in tokenized RWAs such as Treasury Bonds, Corporate Bonds, ETFs, and more. Each bToken is 1:1 backed by the underlying asset, which is in custody by a 3rd-party licensed entity and constantly monitored through Chainlink Proof of Reserves.

bTokens are currently available on Ethereum, Polygon, and Gnosis Chain, while the platform doesn’t have and neither plans its native token. Note how bTokens are sold only to eligible professional investors, who have successfully passed KYC. To be considered a professional investor, private individuals must be able to declare that they hold assets of at least CHF 500,000 and have sufficient professional knowledge or experience, or hold bankable assets of at least 2 million CHF.

Although the requirements are really strict compared to other DeFi protocols, the project has a TVL of $47m, proving its product-market fit.

Arcton

With Arcton, investors can invest in startups by participating in startup IPOs. In an IPO tokenized shares are offered to the public, which investors can buy. These shares carry the same rights as traditional company shares. Specifically, shareholders receive dividends and participate in the sale proceeds of the company.

The protocol opens up doors to startup investing by tokenizing their shares and allowing users to invest as little as $100. Furthermore, Arcton goes beyond traditional crowdfunding by allowing share trading on Camelot's secondary market.

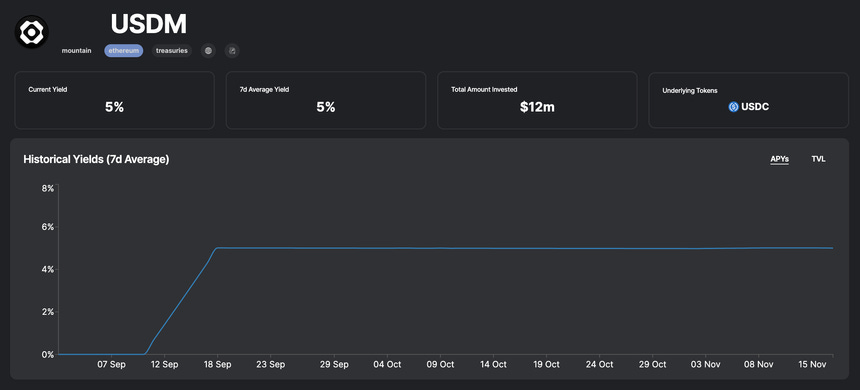

Mountain Protocol

Mountain offers USDM, the first regulated and transparent yield-bearing stablecoin backed by USDM Reserve with JP Morgan as custodian. USDM is fully collateralized by "USDM Reserves" held in segregated, bankruptcy remote accounts. Reserves are composed exclusively of short-term US Treasuries.

Currently, USDM is only supported on the Ethereum blockchain, but the team plans to enable other blockchains in the following months.

USDM can be purchased directly from Mountain Protocol by Primary users, which are those with an active Mountain Protocol account. As for BackedFi, users need to be incorporated businesses in supported countries and comply with the Terms of Service of Mountain Protocol. However, secondary users can acquire USDM from Primary users, from other Secondary users, or via decentralized exchanges.

Regulations & Obstacles

RWAs, as a new phenomenon, are increasingly gaining traction trying to establish connections between DeFi and TradFi. However, they are encountering challenges, particularly in relation to regulations.

In the pursuit for tokenization of Off-Chain Assets (OCA), the liquidity to enable billions of trading volumes will come from TradFi institutions, but there's a problem.

These entities won't enter the space mainly due to the lack of regulations and the current risk implied with smart contracts.

So, at the moment, it's hard to imagine RWAs being traded on the blockchain, as smart contracts are always at risk of being hacked.

The obvious solution at the moment relies on intermediaries in the form of regulated custodian providers such as Coinbase, Bitfinex, Gemini, and banks that provide centralized methods for asset managers to diversify their investments in crypto assets and tokenize their OCAs.

Furthermore, most of the new DeFi startups in the sector are also setting their operations in countries with defined laws to not encounter potential problems in the future and be able to target tradFi entities easily.

Switzerland seems to be the country where most DeFi projects are positioning their headquarters, as the country has provided clear legislation, the Swiss DLT Bill, in 2021.

The fundamental concept conveyed by the law can be boiled down to a simple formula: when it comes to this context, the term "security" is synonymous with "token."

A security grants its holder a specific right against the issuer. For example, a share gives its holder (the shareholder) the right to a dividend against the corporation (the issuer). Securities are usually issued as physical papers. Thanks to the DLT Bill, securities previously issued as paper can now also be issued as a token. In this way, a share certificate becomes a share token, while the rights remain the same.

Another country putting effort into providing a clear regulatory environment is the United Arab Emirates. Since the early days, the UAE government has taken a proactive approach, becoming a magnet for companies looking to create innovative products by leveraging cryptocurrencies and blockchain technology.

2016 - Launch of “Dubai Blockchain Strategy” to improve government efficiency

2018 - Launch of “Emirates Blockchain Strategy 2021” to become the world leader in blockchain adoption

The clear regulatory environment of the UAE is the primary reason for its attractiveness to crypto companies. Something that still lacks in most of the countries around the world.

DMCC (Dubai Multi Commodities Centre) - Allows companies to trade cryptocurrencies.

DMCC Crypto Centre - Specialized business hub for blockchain and crypto startups.

DIFC (Dubai International Financial Centre) - Independent free-trade zone with its regulatory framework for crypto companies.

VARA (Virtual Assets Regulatory Authority) - An entity overseeing the regulation, licensing, and governance of cryptocurrencies, NFTs, and virtual assets.

Abu Dhabi’s tech ecosystem Hub71 has started a massive $2 billion initiative to fund Web3 and blockchain technology startups in the UAE.

These efforts have paid off as some of the world’s leading Crypto exchanges such as Binance, Crypto.com, and Bybit, have set up shop in UAE.

All European countries are also taking steps further to provide a regulated environment for crypto traders and companies, as they're finally rolling out the MiCa regulations this year.

Any company seeking to offer crypto services within the bloc – whether that’s custody, trading, portfolio management, or advice – will need to be authorized by one of the EU’s 27 national financial regulators. Any company offering crypto assets to the public will also need to publish a white paper that is fair and clear, warning of risks without misleading potential buyers. However, by being licensed, crypto providers will get a “passport” to operate across a total addressable market (TAM) of 450 million people.

How could the Sector Evolve in the Future?

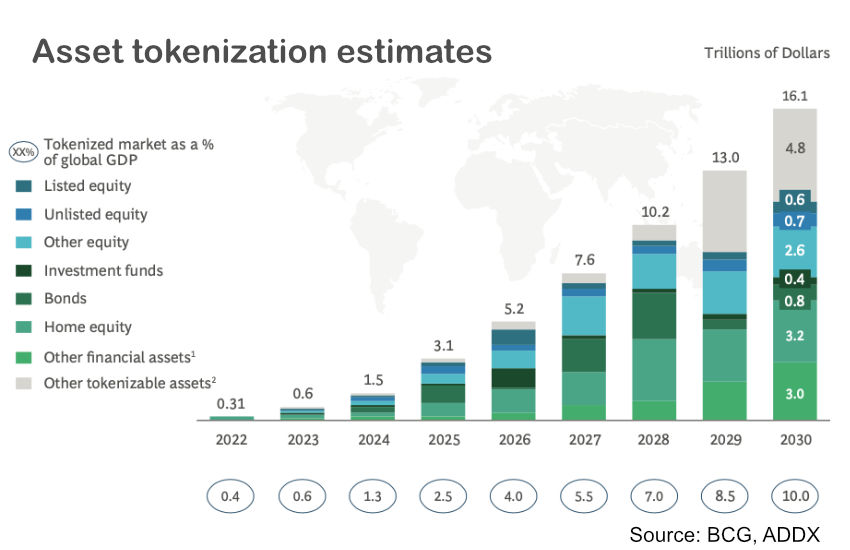

Based on a report by the Boston Consulting Group, tokenized assets are estimated to be a US$16 trillion market by 2030.

This would make up 10% of global GDP by the end of this decade, a significant increase from $310B in 2022.

This estimate includes:

1. On-chain asset tokenization (more relevant to the blockchain industry)

2. Traditional asset fractionalization (e.g., exchange-traded funds (“ETFs”)

3. Real estate investment trusts.

Considering the potential market size, even capturing a small percentage of the market would be a boom for the blockchain industry.

Even with a market size of $16T, tokenized assets would still be a small fraction of the current total global asset value, estimated to be worth $900T – less than 1.8%, to be exact, and not factoring in future global asset value growth.

In 2024, we expect more institutions to partner with established DeFi protocols and teams. This partnership approach helps minimize risks related to counterparties and smart contracts while providing access to on-chain liquidity. We also anticipate a gradual increase in KYC verification integrations inside DeFi protocols to meet regulatory requirements.

Initiatives like Avalanche Evergreen Subnet and Coinbase's layer-2 network Base, which properly accommodate institutional needs and are vertically built on this front, will likely drive the expansion of the RWA industry over the next year. Project Guardian, led by the MAS, is another advanced and relevant case of increased institutional adoption of blockchain-based technologies. It serves as a controlled environment for financial institutions and FinTech companies to experiment with and learn about the application of blockchain and DeFi technologies.

During a pilot event, major players like JP Morgan and SBI Digital Asset Holdings engaged in foreign exchange and government bond transactions using tokenized liquidity pools, setting a new precedent in the financial industry.

Overall, we expect institutional interest in tokenization to persist into the next crypto market cycle as the benefits (capital efficiency, faster settlement, increased liquidity, reduced transaction costs, improved risk management) have become abundantly clear.

Bibliography and Sources

Use our referral system to spread the word about the Chronicle!

Brought to you by Mooms.

Thanks for reading, please follow us on Twitter at @Castle__Cap and visit our website to learn more about our services and get in touch.

Virtually yours,

The Castle

The Alpha Assembly

Receive Telegram notifications of our posts and those of our partners! Join the Alpha Assembly Telegram channel today!

The central hub for everything crypto:

High-level on-chain capital movements

Web3 gaming insights

DeFi research and strategies to give you an edge

Covering everything NFT related: collections, tools, NFT-fi, you name it

News, alpha, and on-the-pulse-content

Reply