- The Castle Chronicle

- Posts

- A Comparative Analysis of Arbitrum’s Positioning within the Layer 2 Landscape

A Comparative Analysis of Arbitrum’s Positioning within the Layer 2 Landscape

Francesco

February 04, 2025 • Est. Reading Time: 11 minutes

Mirror mirror on the wall, who’s the best Layer 2 of them all?

Arbitrum has established itself as a leading Layer 2 (L2) solution, characterized by its advanced technical architecture, well-developed DeFi ecosystem, and a dynamic, composable network.

However, the L2 sector remains highly competitive, and the impending launches of competitors such as Berachain, Monad, and MegaETH could potentially divert significant market share and user attention away from Arbitrum.

Rather than being self-absorbed and talking to ourselves in the mirror, let’s see how Arbitrum is doing compared to other L2 ecosystems.

This report does so through a comparative analysis of Arbitrum’s position relative to other leading L2 ecosystems—Base, Optimism, Mantle, and Blast—leveraging on-chain data to contextualize its current standing.

L2 Key Differentiators

Before diving into our analysis, we introduce each of the L2 selected, with a primer on where they are and where their focus currently lies.

Optimism (OP): Initially launched as a self-standing L2, Optimism has shifted its emphasis from its rollup to the “Superchain,” which has proved very successful and hosts protocols such as Base, Kraken, and Mode. This shift is reflected in their strategic focus and on-chain metrics, prioritizing activity on the Superchain networks rather than the OP L2. The Superchain is the final horizontal scalability vision for Optimism: merging all OP chains into a unified network with shared security and governance.

Base: As Coinbase’s L2 solution, Base benefits from seamless onboarding and a user-friendly ecosystem, positioning itself as a competitor to Solana. The Base network is one of the biggest success stories of L2 and has managed to carve its own space within the competitive landscape. Being backed by Coinbase is indeed a differentiating factor in terms of resources at their disposal, an already existing user base, and the public they can onboard. Being able to capture new narratives timely and positioning early in the AI space has contributed to Base’s growth since its launch.

Mantle: Mantle employs a modular architecture to enhance scalability but lacks the ecosystem maturity of Arbitrum. Nevertheless, with one of the most significant treasuries in the crypto space and a well-developed Liquid Staking Token (LST) ecosystem, Mantle continues to demonstrate growth, as evidenced by its metrics. One of the initial focus of Mantle has been on mETH, their own LST. This has paid off, accumulating over $1.46b in TVL for mETH. While Mantle’s launch has been less than ideal, they are experiencing renewed growth in 2024.

Blast: To incentivize TVL growth before launch, Blast implemented a mechanism that linked network deposits to staked ETH yields. Although initially successful, this model struggled to retain liquidity post-launch. At present, its most successful protocol is Fantasy Top, which integrates SocialFi and gaming. Blast has been unable to capitalize on the launch of its token $BLAST and retain users. Most of the activity onchain appeared to be coming from users intending to mine the incentives offered by Blast and eventually moved to other networks. Blast has recently renewed its focus on a mobile app, bringing a new offer for over 50% APY onchain.

Aside from having different strategic priorities, L2 also feature different governance structures:

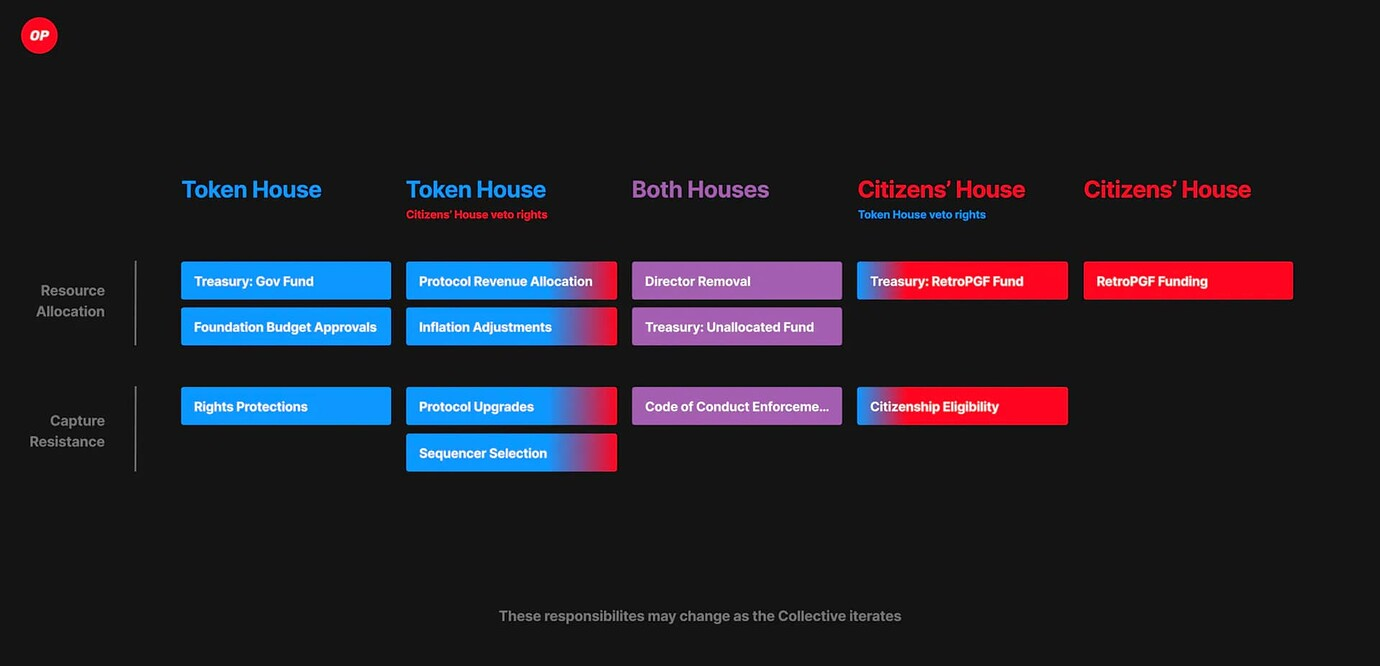

OP is governed by the Optimism collective, composed of users, communities, and applications that contribute to the future of OP.

The collective operates through two “chambers”, the Token House and the Citizens House, with different responsibilities:

Base is currently led by a centralized team: it is only possible to speculate on a potential future token and whether it will eventually have governance rights, but currently, Base is operated by a centralized team.

Mantle’s governance is decentralized, with $MNT token holders able to delegate their governance power, participate in the forum, and vote on proposals on Snapshot. While the initial Mantle Implementation Proposals (MIP) had good traction in the forum, governance activity has slowed down lately.

Blast follows a similar model to Mantle, with $BLAST tokeholders able to participate in discussions and vote proposals on the Blast forum. However, what is in their powers has to follow the bylaws defined in the Blast docs clearly.

Lastly, Arbitrum governance is also decentralized and led by the Arbitrum DAO, with $ARB token holders able to participate in the decision-making process and vote on proposals. The Arbitrum DAO is the biggest and one of the most active in the sector.

These different governance forms also impact how L2s have performed since launch. Having a top-down governance structure prioritizes efficiency and pace of development. However, it can lead to misalignment with the community and a lack of decentralized decision-making and engagement. On the other hand, complete decentralized governance might lack the efficiency of its centralized counterpart while ensuring community participation and shared decision-making.

What makes Arbitrum Unique?

Arbitrum’s unique value proposition is a unique combination of:

Tech Stack

Performance

User adoption

With the initial purpose of L2 being enhancing the scalability of Ethereum, Arbitrum has solidified itself as one of the fastest and cheapest L2 solutions.

This is a reflection of Arbitrum’s super performant stack, allowing:

Fast Block Times: Arbitrum One produces blocks every 250 milliseconds, significantly enhancing user experience (UX) with faster transaction confirmations. Orbit chains can be configured with block times as low as 100 milliseconds. These block times also make Arbitrum more efficient by reducing the value extracted by arbitragers and more attractive to institutional investors, who required low latency.

Multiple programming languages with Stylus: Stylus introduces a second virtual machine (WASM VM) alongside the traditional Ethereum Virtual Machine (EVM). This allows developers to write smart contracts in languages like Rust, C, and C++, rather than being limited to Solidity. Stylus offers cheaper execution, enhanced security, and interoperability between different programming languages.

Security-First Approach: As one of the first Stage 1 L2s (as per L2Beat), Arbitrum emphasizes robust security measures to stimulate trust in its ecosystem.

The development of upgrades like Stylus, Timeboost (which we will dive into later), and BOLD (decentralizing validation) continues to show the defining traction of Arbitrum’s tech stack in making it a leading L2. While a strong technical foundation is essential, the true metric of success lies in user adoption, measured by how many users are willing to pay gas fees to utilize the network.

Part of Arbitrum’s initial success stemmed from its thriving DeFi ecosystem, including projects like GMX, Gains as perpetual exchanges, and Dopex (now Stryke) for options. Users migrated to Arbitrum for its affordability, speed, and diverse application offerings.

However, remaining a leader in the sector requires continuous adaptation. As L2s have solidified as the chosen scalability solution for Ethereum, tens of new blockchain networks launch daily. Just like the landscape changes, so does the behavior of users

As attention has become a scarce commodity. L2s must solidify and reinvent their value propositions to capture and retain mindshare. This includes strengthening key verticals and staying flexible enough to attract new innovative primitives and compete with others.

According to data provided by Defillama, Arbitrum ranks:

6th by TVL

3rd by the number of protocols.

6th in active addresses, exceeding 200k.

5th in stablecoins, with $5 billion (data from Artemis.xyz)

5th in 24-hour transaction volume, surpassing $870 million.

How does this compare with other L2?

And how has this evolved and changed since Arbitrum’s launch?

The following section dives into these metrics using on-chain data, comparing Arbitrum to other leading L2, including:

Base

Optimism

Mantle

Blast

Focusing on Metrics That Matter

To streamline the comparison, Arbitrum’s positioning in the L2 space can be evaluated by analyzing key metrics such as:

Total Value Locked (TVL)

Daily Active Addresses

Stablecoin supply

DEX volumes

Fees generated

These indicators provide a clear view of user adoption and ecosystem growth.

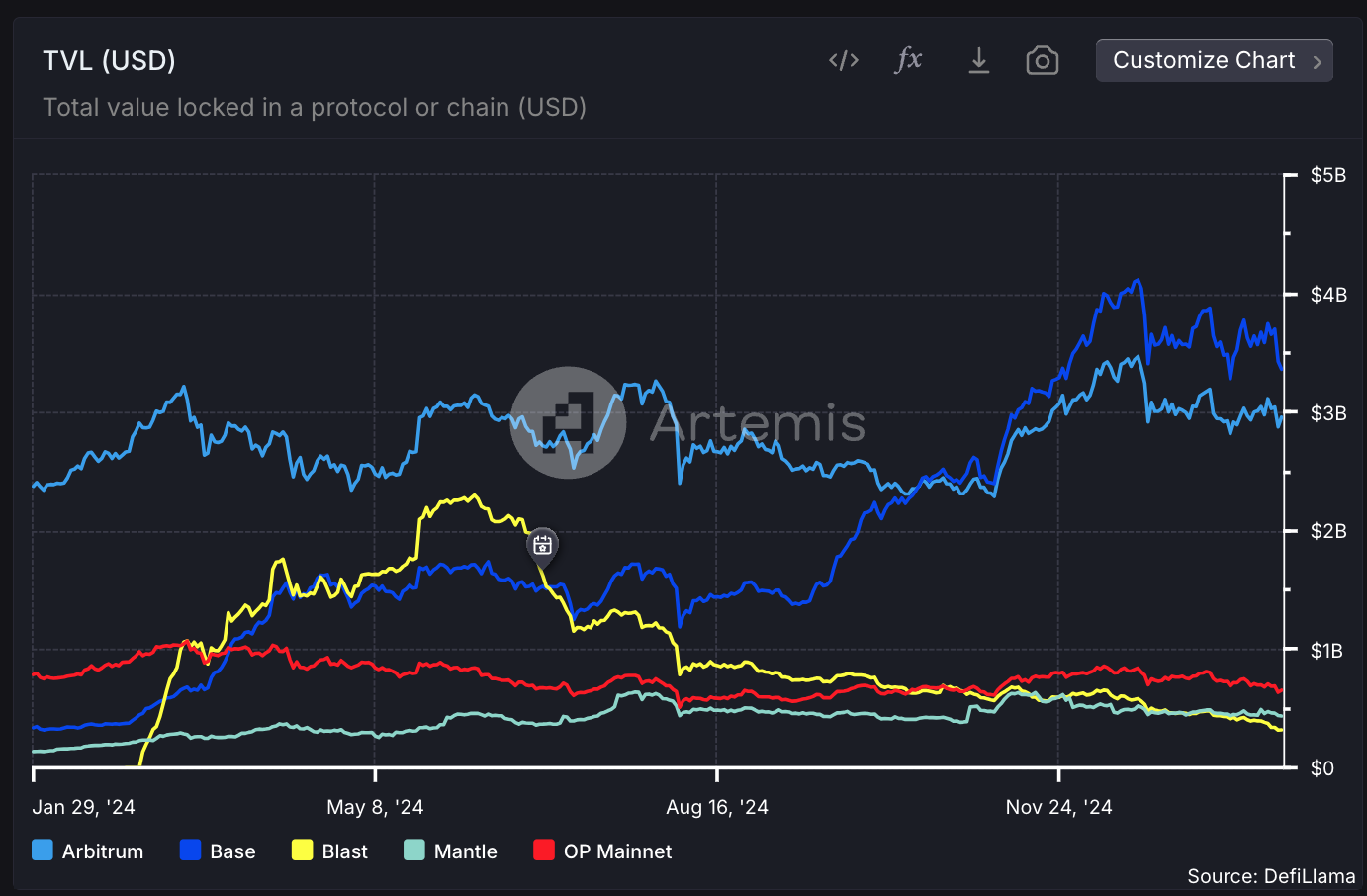

1. Total Value Locked

TVL indicates ecosystem health, highlighting users' willingness to deposit their liquidity in a specific chain. As such, it can be interpreted as a proxy for adoption.

Until October 2024, Arbitrum was the leading L2 in terms of TVL. Nowadays, Base leads the pack with $3.6b, followed by:

Arbitrum at $2.9b

OP at $656k

Mantle with $445k

Blast with $322k.

The chart shows how L2 are following different paths, which are reflected in their TVL:

Arbitrum and Base are self-sustaining, outperforming and growing TVL compared to Q2 2024

Base more than doubled its TVL in the last 6 months of 2024

Given the strategic decision of OP to focus on the Superchain, the TVL is not seeing significant growth

Mantle has shown traction, growing its TVL from Q2 2024

Blast is facing an identity crisis as the TVL on the chain has crashed post-TGE

The significant surge in TVL on Base can be attributed to the success of Aerodrome, which reached over $1b in TVL, and the launch of Morpho Blue, which gathered over $831m in TVL.

Here are the top 10 protocols by TVL on Base and Arbitrum, as reference:

Base: left, Arbitrum: Right

New lending markets and attractive veTokenomics are only some distinctive applications that have found enormous success on Base.

If we exclude the top protocol for each chain (Aero, AAVE), the other four protocols on Base contribute $2.5b in TVL, while Arbitrum’s top 2-5 only add $1.2b.

If Arbitrum wanted to replicate this blueprint, it would require:

Reducing its TVL dependency on AAVE

Positioning as the most attractive marketplace for established protocols looking to expand (e.g. Aero, Morpho)

Incentivize native solutions

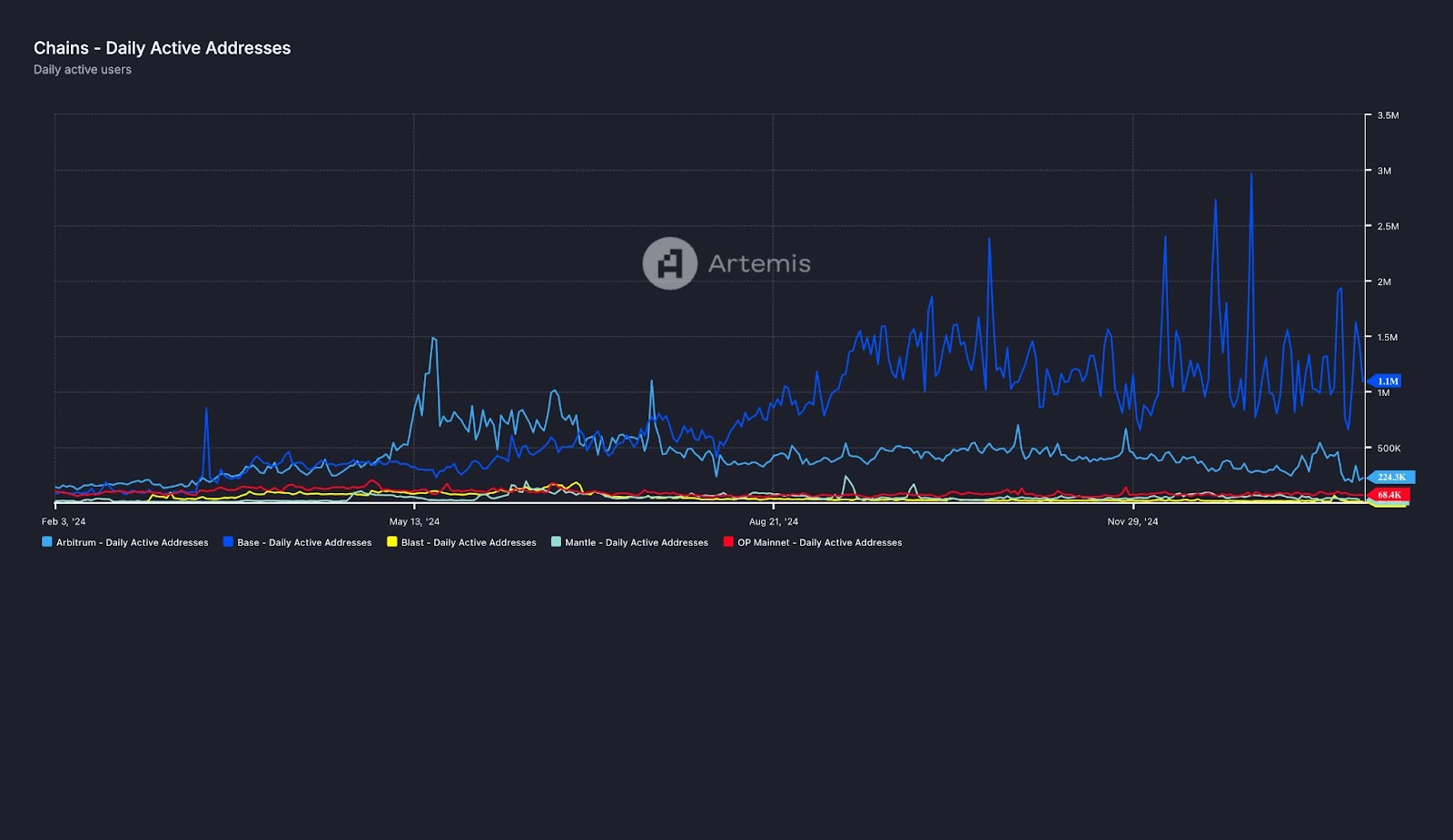

2. Daily Active Addresses (DAA)

The use of daily active addresses to compare blockchain networks is highly discussed.

While DAA is often used to measure user engagement, it can be misleading due to inflated activity from low-value transactions.

In this report, we mainly use it as a counterargument to the fact that Arbitrum lacks traction and is being eclipsed by the numbers of others, especially Base.

7-Day Average DAA:

Base: 1.3M

Arbitrum: 428K

Optimism: 89.1K

Mantle: 37.9K

Blast: 27.6K

This underlines a significant difference: on paper, Base has almost 4x the number of Arbitrum users.

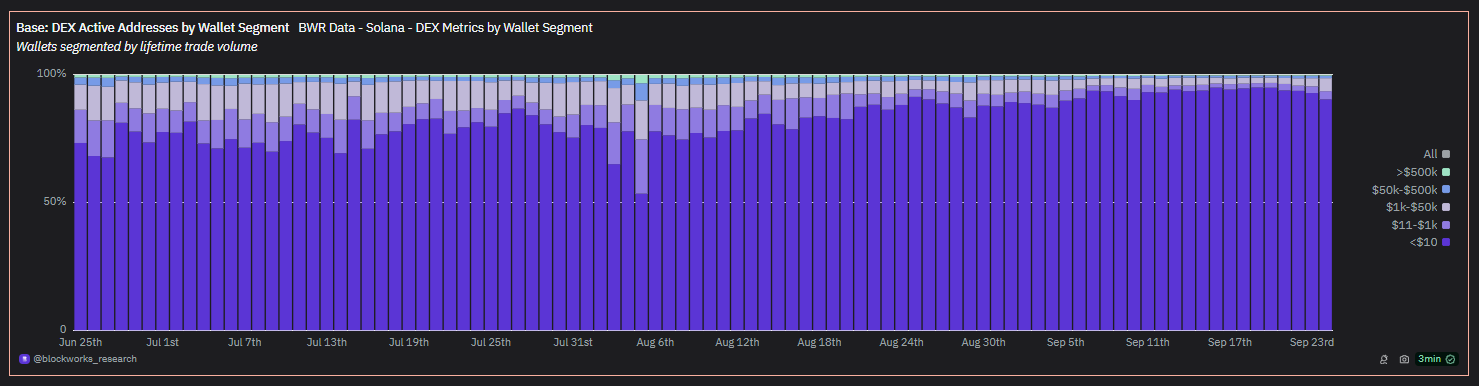

Nonetheless, Blockworks and others have pointed out the fallacy of measuring daily active users several times. Researching Solana, they discovered that “When segmenting active addresses (traders) by their lifetime volume, over 80% of active addresses trade less than $10 of volume”.

When looking at the same metric for Base, they found out this applied to over 90% of addresses (data until September 2024).

While these users might still have a good wallet value, these examples show that daily active addresses are not a reliable metric for actual blockchain usage and should be taken with a grain of salt.

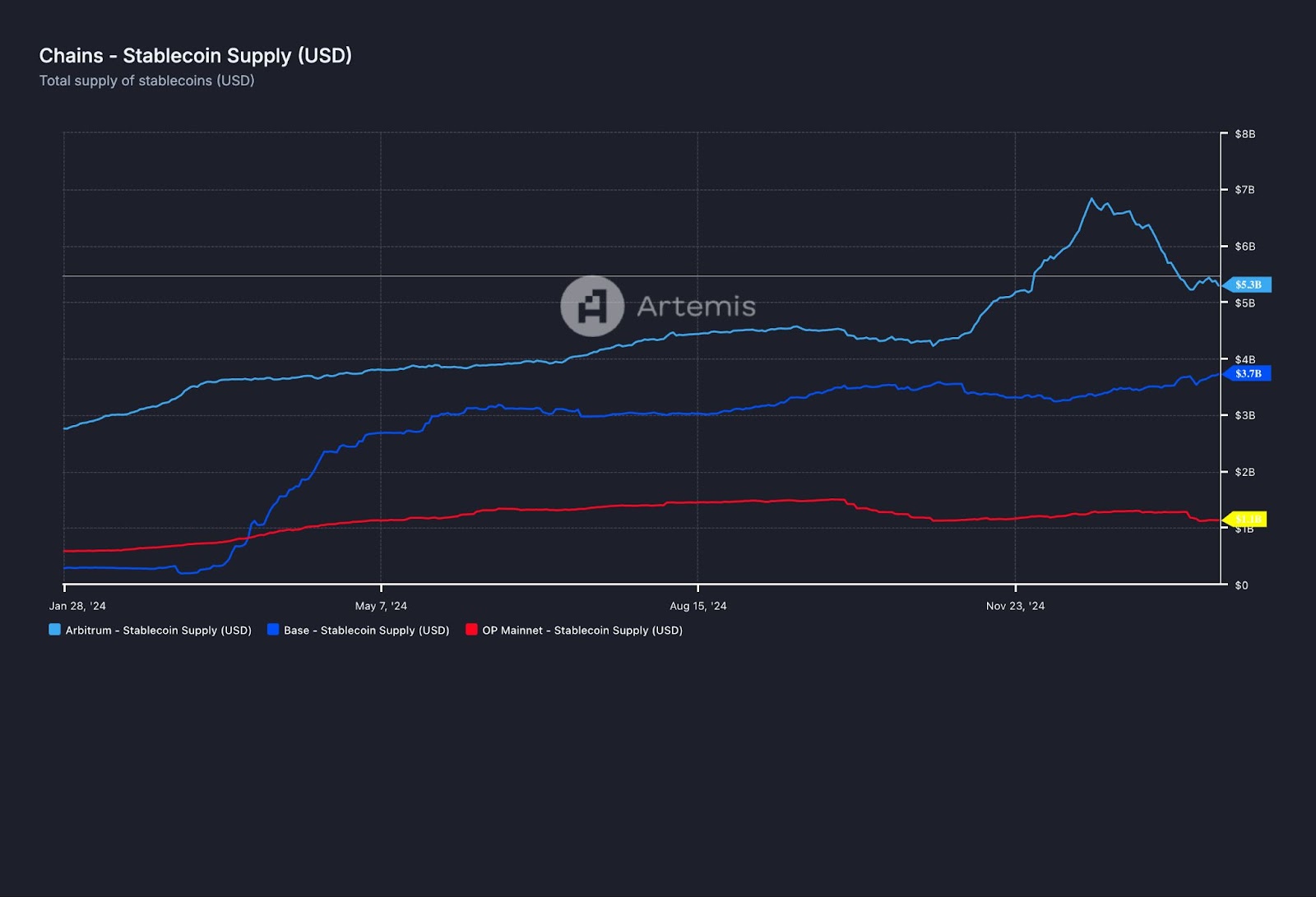

3. Stablecoin Supply

Stablecoin liquidity is critical to a thriving DeFi ecosystem, enabling users to engage with lending protocols and liquidity pools.

Even after excluding the USDC deposited in the Hyperliquid bridge, Arbitrum is the leading L2 for stablecoin supply, with $5b compared to Base $3.7b.

Data for Mantle and Blast has been complemented using Defillama:

Mantle: $397m, a very good result considering they started bootstrapping TVL from November 2023. Mantle has more than doubled the stablecoin supply onchain compared to July 2024.

Accommodating a strong Stablecoin Supply shows ecosystem maturity and availability to cater to retail and institutional investors.

The stablecoin market, in general, is also experiencing a renaissance, with new models such as Ethena, Usual, and Resolv challenging incumbents stablecoins like USDT and USDC.

To attract more stablecoins, Arbitrum has to continue to deepen its leadership within DeFi and double down into new native innovations that can complement the more established ones.

Tying this with the previous TVL comparison, launching new lending markets like Morpho, and accommodating more Liquid Staking Tokens and Liquid Restaking tokens would be two great starting points.

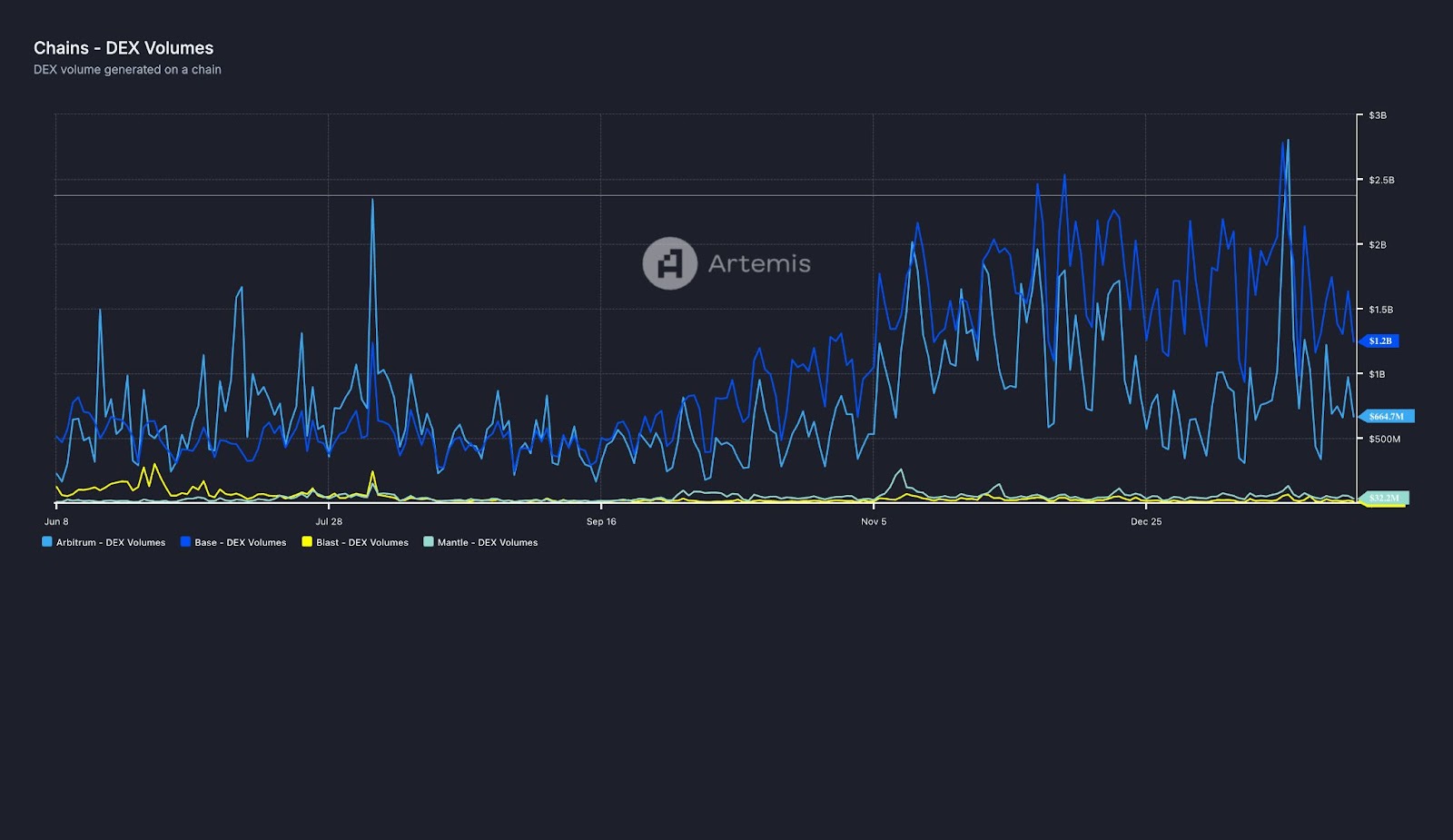

4. DEX Volume

DEX volumes provide insights into liquidity and trading activity within an ecosystem.

The data in the chart below resembles the previous metrics, identifying two clear blocks: Base and Arbitrum leading and everyone else much below.

The data was selected starting in June 2024 to avoid a spike in volume on the Blast chain.

Nonetheless, observing the chart, we can notice that DEX volumes have been down for all L2 during the past few weeks. A few reasons for this can be attributed to the market dump of the last weekend, allegedly caused by DeepSeek and the fear of tariffs imposed by Trump.

Base surpassed Arbitrum in DEX volume in September 2024, driven by Aerodrome’s rapid growth, which saw volumes rise from an average of $2.8 billion weekly in September to an all-time high of $8 billion in December 2024.

This is almost as much as Arbitrum does weekly:

Here’s how Arbitrum and Base’s top 10 DEXs compare:

Base: Left, Arbitrum: Right

On Arbitrum, Uniswap dominates DEX activity, accounting for over 50% of weekly volume ($4 billion, or 50% of Total Volumes), followed by Camelot ($858 million) and PancakeSwap ($451 million).

On the other hand, while Uniswap leads on Base as well, Aerodrome has surpassed it for weekly volumes, with over $4.93b compared to Uniswap’s $4.28b.

Arbitrum’s reliance on Uniswap highlights the need to diversify.

Aside from this notable difference, most of the other protocols perform similarly.

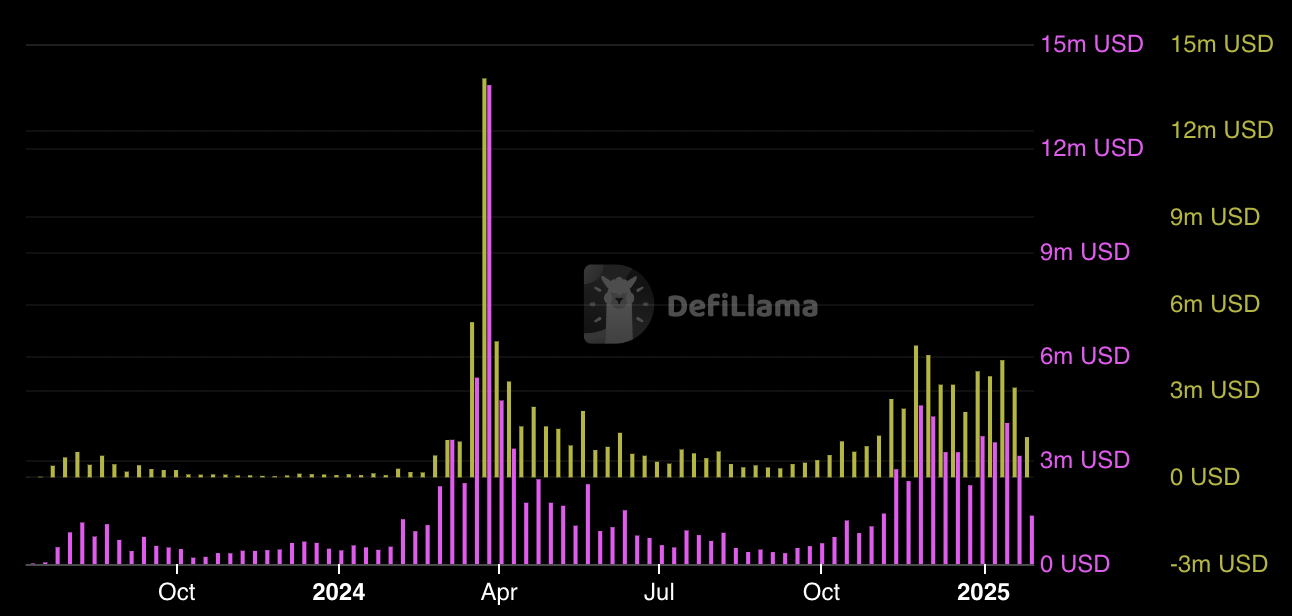

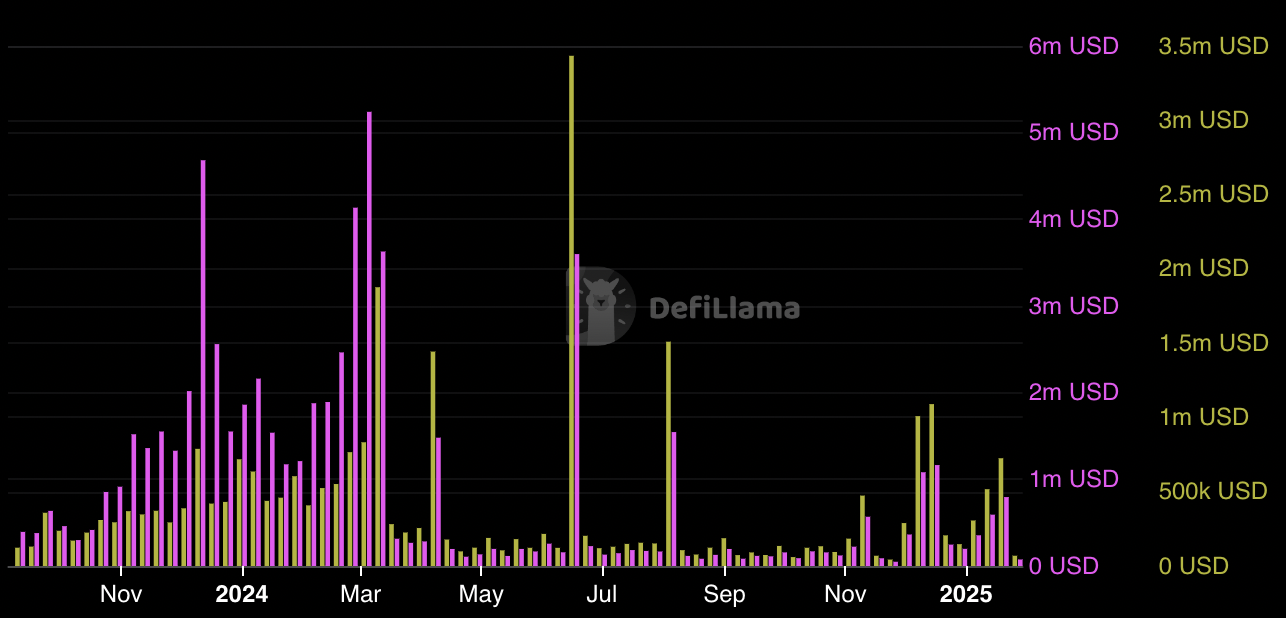

5. Fees Generated

Fee generation reflects L2’s capacity for financial sustainability: L2s have limited elements to generate fees - so maximizing revenues from them becomes critical.

The increase in fees generated by base starting from September 2024 can be attributed to the increasing volume of transactions onchain, which we have shown above. As fees have a flexible component, they also adapt to demand.

Furthermore, Base has a higher base fee for its transactions than Arbitrum and other L2s.

When analyzing the fees generated by Base and Arbitrum, the contribution of a higher base fee becomes evident.

The first chart below here highlights the Base weekly fees generated:

The chart below looks at the same metric for Arbitrum. We can observe how the introduction of EIP-1559 has drastically reduced transaction costs across L2s and, consequently, reduced their fees and revenues. During the past few weeks, Arbitrum has struggled to read $1m in fees generated weekly, while Base has consistently generated over $5m for several weeks in a row.

Arbitrum is exploring revenue-enhancing mechanisms like Timeboost, which uses auctions to determine transaction ordering. Increasing base transaction fees could also provide additional financial stability with minimal impact on user experience.

Challenges and Opportunities

Challenges

Competition: The emergence of high-profile competitors like Berachain, Monad, and MegaETH poses a direct challenge to Arbitrum’s market position.

User Retention: As new networks launch with attractive incentives, retaining users and developers will require continuous innovation and engagement.

Evolving Narratives: Staying relevant in an industry driven by hype and rapid technological shifts demands adaptability and proactive storytelling.

Decentralization: moving Arbitrum to Stage 2 Rollup, Decentralizing the sequencer, and more.

Opportunities

Arbitrum needs to innovate its ecosystem, which has always been its value proposition: integrating new lending markets and developing native applications are some competitive points that could strengthen Arbitrum’s positioning.

Reducing dependence on Uniswap is critical. The recent partnership between Camelot and Offchain Labs is a sign that this is a shared sentiment.

Generating more fees should also be considered another priority: increasing the base fee has been previously explored within Arbitrum DAO’s working groups and could be further analyzed.

Growing institutional interest in Arbitrum should also be leveraged: the STEP program has bootstrapped Arbitrum’s RWA TVL to over $100m. Developing more protocols to accommodate these providers is fundamental to capitalize on and appropriately meet investor demand.

Expansion into New Verticals: Opportunities in gaming, NFTs, and enterprise solutions can unlock new growth avenues beyond DeFi.

Following trends and being able to act quickly on them with conviction and not lag: welcoming new narratives and allowing them to capitalize on Arbitrum’s composable ecosystem.

Arbitrum still leads in stablecoin supply, although Base has surpassed it across most of the metrics analyzed.

Arbitrum metrics are still growing and are not in a downtrend. From a tech and ecosystem perspective, Arbitrum is solidifying its position as one of the most complete L2 solutions.

Tailoring to existing protocols looking to expand, or to new assets, and adding key applications to the ecosystem in verticals that need them. Some coming to mind include LSTs, LRTs, and AI.

Food for Thought and Conclusion

Arbitrum has firmly established itself as a leading Layer 2 solution, driven by its superior tech stack, a robust DeFi ecosystem, and strong user adoption. However, the landscape introduces new challenges as competitors like Base, Optimism, Mantle, and Blast continue to gain traction.

The upcoming launch of networks such as Berachain, MegaETH and Monad adds to the competitive pressure, necessitating a proactive and strategic approach to maintain market leadership.

The data reveals that the sample of L2 analyzed can be categorized into two blocks. The leading one, with Base and Arbitrum becoming self-sustaining and growing their metrics, and the lagging one, where:

OP is deliberately focusing more on the Superchain ecosystem and, as such, is not focusing on its metrics.

Blast is struggling post-TGE, with most of the metrics showing little to any rebound from the downtrend.

Mantle has failed to capitalize on its launch to attract mindshare but has consistently improved across all metrics in 2024 and is poised to continue on this growing trajectory.

Within this context, Arbitrum emerges as a growing L2, with several points from improvements and lessons to be learned from the success of its competitors.

Despite being surpassed by Base in several key metrics, such as TVL and DEX volumes, Arbitrum remains dominant in areas like stablecoin supply and ecosystem composability.

By continuing to innovate, reducing dependency on dominant protocols like Uniswap for DEX, and fostering new native applications, Arbitrum can strengthen its ecosystem and retain its competitive edge. Additionally, exploring opportunities to diversify into emerging verticals, increasing revenue through mechanisms like Timeboost or adjusting base fees, and leveraging institutional interest can position Arbitrum for sustained growth.

The metrics analyzed in this report underscore the need to be agile and adaptable in an industry defined by rapid change.

While the competition intensifies, Arbitrum’s solid foundation, commitment to innovation, and ecosystem flexibility make it well-positioned to thrive as a leading L2.

Brought to you by Francesco

Thanks for reading, please follow us on Twitter at @Castle_Labs and visit our website to learn more about our services and get in touch.

Virtually yours,

The Castle

The Alpha Assembly

Receive Telegram notifications of our posts and those of our partners! Join the Alpha Assembly Telegram channel today!

The central hub for everything crypto:

High-level on-chain capital movements

Web3 gaming insights

DeFi research and strategies to give you an edge

Covering everything NFT related: collections, tools, NFT-fi, you name it

News, alpha, and on-the-pulse-content

Reply